Cement companies are set to report healthy operating profitability of ~20% next fiscal on an expected recovery in demand driven by the infrastructure and affordable housing sectors, stable realisations, and benign input prices.

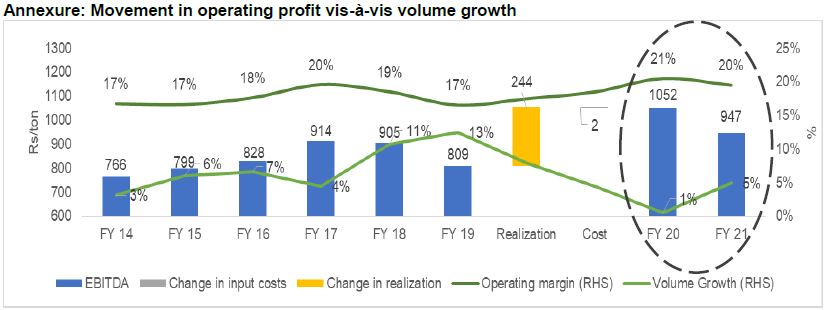

This fiscal, operating profitability is expected to touch a 7-year high of ~21%, which translates to a 350-400 basis points (bps) on-year surge.

Says Hetal Gandhi, Director, CRISIL Research, “Next fiscal, we anticipate volume growth recovering to 5-6% from 0.5-1% estimated for this fiscal. Demand growth in the infrastructure and affordable housing sectors on a lower base should support volume growth. These two sectors together contribute almost 35-40% of cement demand in India.”

Cement prices are expected to remain stable in fiscal 2021 after high volatility seen this fiscal. The expected recovery in demand and high utilisation of clinker capacities at 78% -- because new capacity additions are skewed towards split grinding units – would restrict any steep decline in cement realisations.

We foresee input prices also remaining range-bound over the medium term, amid stable coal prices and downward pressure on crude oil and petcoke prices, though there could be short-term volatility.

The high profitability this fiscal has been driven by an estimated 5% growth in cement prices and softer input prices (lower petcoke and coal prices resulted in a 6-7% decline in power and fuel costs. This has largely offset adverse movements and fluctuations in the prices of other inputs). This was despite slower demand growth during the fiscal, owing to lower spending by government departments and overall economic slowdown.

Our analysis of 19 listed cement makers with revenue of over Rs 500 crore (comprising 70% of industry capacity) shows large players are more resilient to demand slowdown as their volume growth is estimated at ~2% this fiscal, or higher than the industry average.

Consequently, the credit profiles of large cement makers have witnessed an improvement this fiscal after exhibiting resilience over the past few years despite cost pressures, supply-side challenges, and heightened M&A activities due to ample liquidity and sound balance sheets.

Says Nitesh Jain, Director, CRISIL Ratings, “The credit profiles of cement makers next fiscal should continue to mend. Net debt/EBITDA is set to improve to ~1.7 times this fiscal from ~2 times in fiscal 2019, and further to ~1.6 times next fiscal driven by healthy operating profitability, moderate capex and strengthening balance sheets.”

The industry’s annual capex is seen at Rs 9,000-11,000 crore in fiscals 2020-2021, in line with the past trend.

Release of funds for key infrastructure projects and transmission of interest rate cuts are important to demand recovery and pricing sustenance.

Mumbai

Mumbai