Securitisation volume, which had surged nearly 50% in the first half of last fiscal, was yanked back in the second half as the economy slowed and Covid-19 pandemic spawned risk aversion.

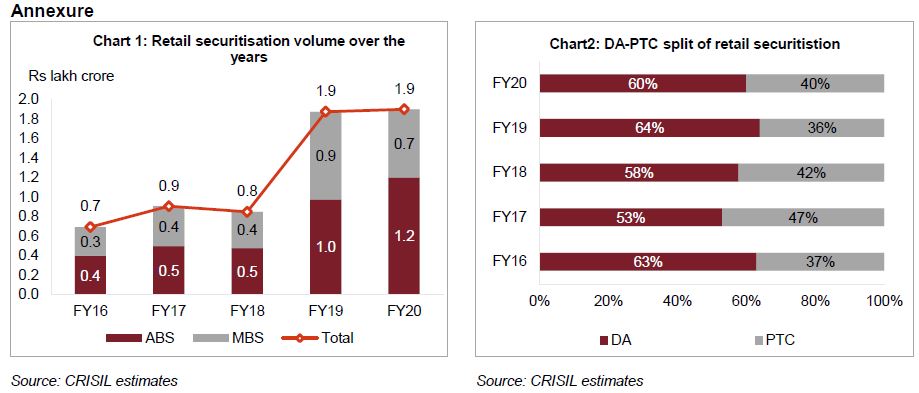

Consequently, securitisation volume ended flat at Rs 1.9 lakh crore in fiscal 2020 (see chart 1 in annexure), with transactions falling off the cliff in March. An uptick in asset backed securitisation (ABS) lent some support, with the number of originators rising past 130 from just over 100 in fiscal 2019.

Says Krishnan Sitaraman, Senior Director, CRISIL Ratings, “There was a sudden meltdown in volume last fiscal in March, when transactions typically peak. Pass-through certificate (PTC) issuances, for instance, dropped to around Rs 9,000 crore, compared with Rs 15,000 crore in March 2019.”

Investor interest in ABS transactions grew as newer non-banking financial companies (NBFCs) used securitisation to raise money. Further, after a hiatus of more than a decade, we saw commercial banks starting to actively explore raising funds through ABS. In addition, wider investor acceptance of securitised instruments backed by receivables from newer asset classes such as gold loans, two-wheeler loans and small business loans propped volume.

On the other hand, mortgage-backed securitisation (MBS) volume fell 25% on-year to Rs 70,000 crore. This would have pulled down the overall volume as well, but for a 20% growth in ABS, which accounted for 65% of securitisation volume in fiscal 2020 compared with 52% in the previous one.

To be sure, MBS volume was already diving because some large housing finance companies facing business disruption had curbed their securitisation activity to a fourth of fiscal 2019 levels. Legal interpretation issues related to securitisation payouts involving an originator undergoing insolvency proceedings also dampened sentiment. Direct assignment (DA) continued to dominate, accounting for over 60% of securitisation volume (see chart 2 in annexure). The government’s partial credit guarantee scheme was a key contributor to the increasing popularity of DAs.

Further, higher capital relief for originators under DA transactions after the adoption of IndAS, and banks chasing credit growth in a weak credit environment, propped volume. In addition, DAs remained the preferred route for MBS transactions. However, in a break from the past, barely half of ABS transactions were through PTCs as opposed to over 65% historically.

Looking ahead, near-term headwinds are expected to continue until the nationwide lockdown is lifted and normalcy returns. Any uptick in delinquencies in retail loan portfolios of financiers on account of the economic slowdown or weakening of credit discipline among borrowers would be a dampener.

An important rating driver for existing securitisation transactions in the near term would also be the approach taken by investors in providing moratorium to underlying borrowers and in rescheduling payouts. Not permitting reschedulement could result in downward rating actions in some transactions.

Says Divya Chandran, Director, CRISIL Ratings, “Near-term challenges notwithstanding, securitisation is here to stay as it has been established as a viable alternative fundraising option for NBFCs. A growing pool of large, medium, and small non-banks would continue to tap the securitisation market in an effort to have a diversified resources profile. Further, to mitigate the risks arising from the near-term challenges, PTC transactions with ultimate payment structures – as opposed to the currently prevalent timely payment structures – could be the flavour of the market over the medium term.”

Mumbai

Mumbai