Mumbai

Mumbai

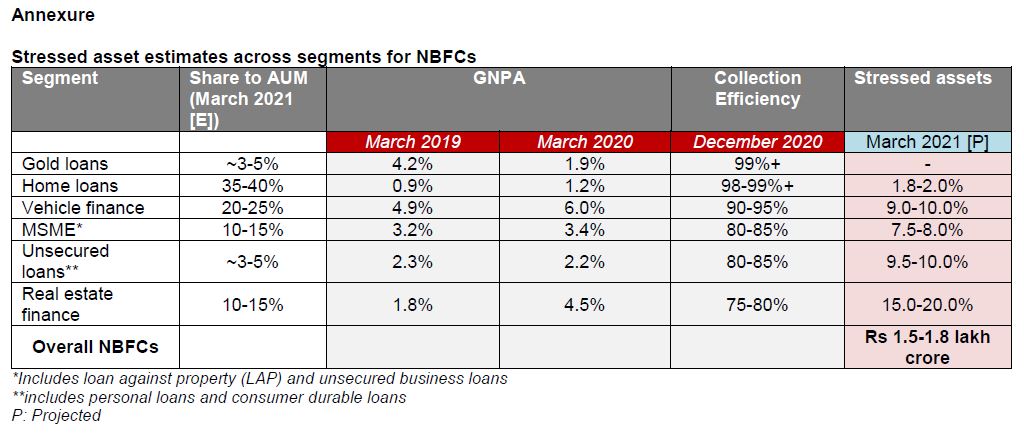

1 Stressed assets = Pro-forma GNPA (including accounts which have not been declared NPA as per Supreme Court order) + potential stress in loan book (including restructuring)

2 Comprising both non-banking finance companies and housing finance companies, excluding Government owned NBFCs

Subscribe for our press releases

Media relations

Saman Khan

Media Relations

CRISIL Limited

D: +91 22 3342 3895

M: +91 95 940 60612

B: +91 22 3342 3000

saman.khan@crisil.com

Analytical contacts

Krishnan Sitaraman

Senior Director

CRISIL Ratings Limited

D: +91 22 3342 8070

krishnan.sitaraman@crisil.com

Ajit Velonie

Director

CRISIL Ratings Limited

D: +91 22 4097 8209

ajit.velonie@crisil.com