The liquidity cover1 available with CRISIL-rated non-banking financial companies2 (NBFCs) will decline sharply if they cannot avail on their own bank borrowings the moratorium announced by the Reserve Bank of India (RBI) in its “COVID-19 Regulatory Package”.

NBFCs face a double whammy because they are offering moratorium to customers despite not getting one themselves from their lender-banks. That will put significant pressure on liquidity profiles of many NBFCs.

CRISIL’s analysis3 of NBFCs it rates shows liquidity pressure will increase for nearly a quarter of them if collections do not pick up by June 2020. These NBFCs have Rs 1.75 lakh crore of debt obligations maturing by then.

With collections minimal and the moratorium only for their borrowers, raising fresh funds is critical, especially because NBFCs, unlike banks, do not have access to systemic sources of liquidity and depend significantly on wholesale funding.

To be sure, Rs 1 lakh crore has been made available through the RBI’s Targeted Long-Term Repo Operations (TLTRO) window. However, only half of that is earmarked for primary issuances. Also, an expected scramble for funds means corporates and government-owned financiers will also be interested in this window. Consequently, only higher-rated NBFCs may end up benefiting.

To boot, mutual funds, a large investor base for higher-rated NBFCs, have been facing redemption pressure and therefore are unlikely to be a material source of fresh funding or refinancing. And securitisation, which many NBFCs were relying on so far, may also not see much transactions in the near term because of the moratorium.

While larger and better-rated NBFCs may still be able to manage the situation, smaller or lower rated NBFCs, which have significant dependence on bank funding, will find the going extremely tough. Measures such as enhancement in bank lines, ad hoc or special Covid-19 credit lines from banks, would offer only a partial relief to the sector.

Says Krishnan Sitaraman, Senior Director, CRISIL Ratings, “Given the challenges in access to fresh funding, and presuming nil collections, CRISIL’s study underscores that a number of NBFCs will face liquidity challenges if they do not get a moratorium on servicing their own bank loans and are forced to meet all debt obligations on time.”

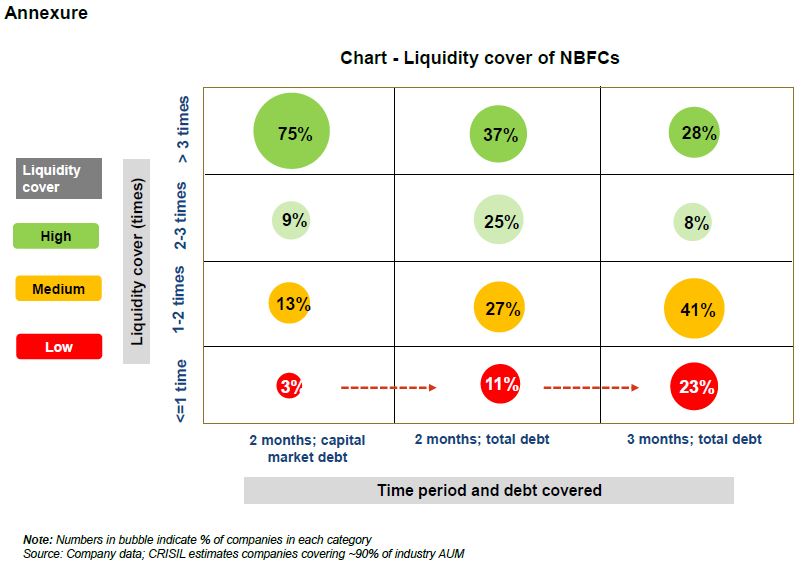

To analyse the issue, CRISIL first evaluated the liquidity position of NBFCs based on the understanding that they would benefit from a moratorium on their bank loans. Under this scenario, CRISIL estimated that almost three-fourths of NBFCs will have a liquidity cover of over 3 times to meet capital market debt obligations up to May 31, 2020, when the moratorium is slated to end. On the other hand, only 3% had less than 1 time liquidity cover (see chart in annexure).

A liquidity cover of less than 1 time indicates inability to make debt repayments on time and in full without the benefit of collections, external support, or access to additional credit lines or funding.

If we assume no moratorium on bank debt, only 37% of the CRISIL-rated NBFCs will have a liquidity cover of more than 3 times for their total debt repayments up to May 31, 2020, while those with less than 1 time would increase to 11%.

And if business disruption continues beyond the moratorium period, considering debt repayments till June 30, 2020, almost a quarter of these NBFCs would have a liquidity cover of less than 1 time with debt obligations aggregating to Rs 1.75 lakh crore.

Realistically, NBFCs expect some funds to come in through collections, but the amount would vary based on asset class. However, it is important to note that even if the lockdown ends, collections are unlikely to return to normal levels immediately and will improve only gradually. Borrower behaviour regarding payment discipline after the moratorium will be a key monitorable.

CRISIL understands that NBFCs are seeking both, clarity from the RBI on applicability of moratorium and access to a formal liquidity window which may provide some structural liquidity support to NBFCs similar to that available for banks.

CRISIL is closely scrutinising the impact of these developments on the credit profiles of NBFCs and will take appropriate rating action where required.

1 Measured as “(Cash available with NBFC + unutilised bank lines) /Debt falling due”

2 Comprising NBFCs, housing finance companies, and microfinance institutions, but excluding government owned non-banks

3 Analysis covers CRISIL rated investment-grade NBFCs, constituting around 90% of industry assets under management (AUM)

Mumbai

Mumbai