Risk Models and Framework

Risk Models and Framework

Our services include

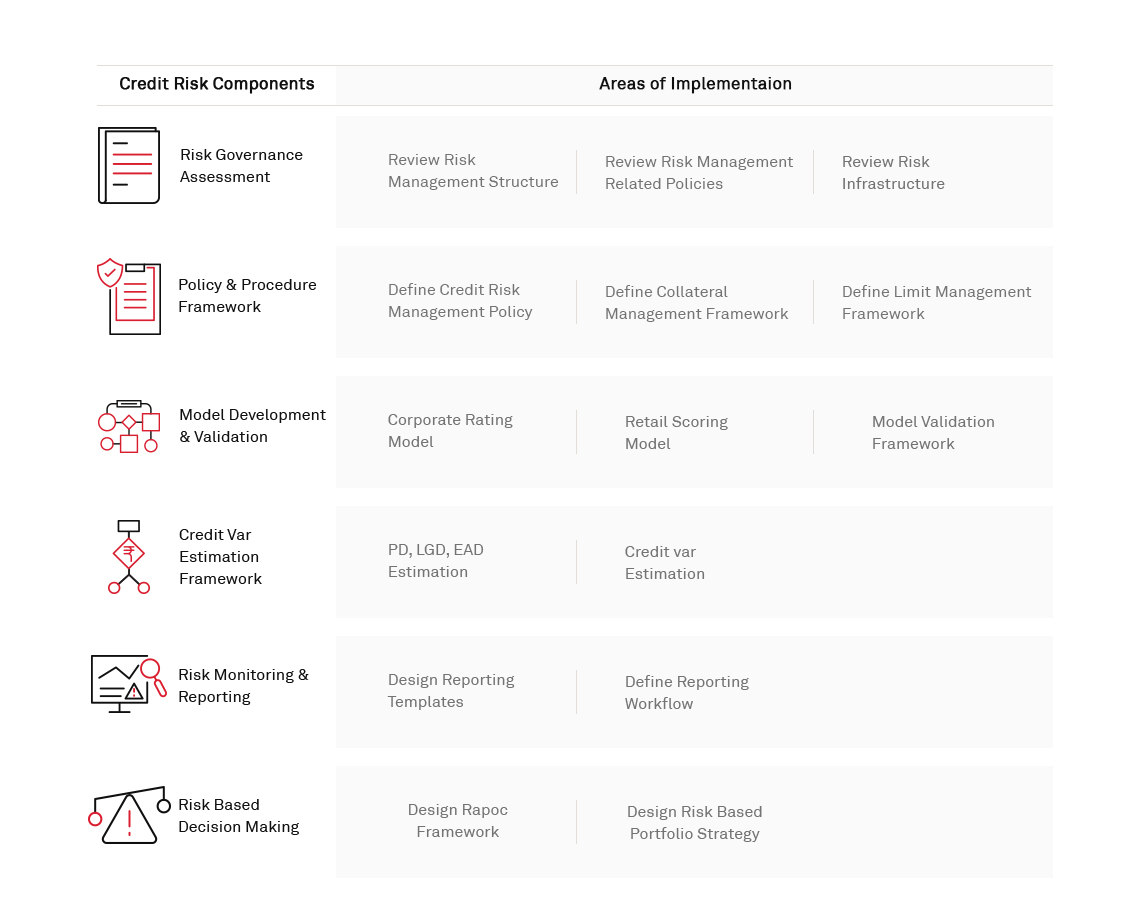

Policy & Procedure

- Design and implementation of a best practices-based credit risk management framework

- Reengineering of credit and credit risk management processes

- Preparation of credit risk management policy

- Design of collateral management framework

- Design of RAROC estimation and risk-based pricing framework

Gap Analysis

- Diagnostic review of credit risk management practices compared with industry best practices and regulatory guidelines.

Model Validation

- Development and validation of internal credit rating models for different categories of borrowers

Model Development

- Development of appropriate corporate and retail risk models for portfolio credit risk management, including an estimate of asset correlations

Parameter Estimation

- Installation of data management processes and analytical methodologies for deriving default probabilities, transition matrix and loss given default statistics

Credit VaR Estimation

- Development of framework to estimate portfolio credit VaR based on underlying parameters, as well as inter-sector correlations

Credit Risk Consultancy

Our services include

Gap Analysis

- Diagnostic review of credit risk management practices compared with industry best practices and regulatory guidelines.

Policy & Procedure

- Design and implementation of a best practices-based credit risk management framework

- Reengineering of credit and credit risk management processes

- Preparation of credit risk management policy

- Design of collateral management framework

- Design of RAROC estimation and risk-based pricing framework

Model Development

- Development of appropriate corporate and retail risk models for portfolio credit risk management, including an estimate of asset correlations

Model Validation

- Development and validation of internal credit rating models for different categories of borrowers

Parameter Estimation

- Installation of data management processes and analytical methodologies for deriving default probabilities, transition matrix and loss given default statistics

Credit VaR Estimation

- Development of framework to estimate portfolio credit VaR based on underlying parameters, as well as inter-sector correlations

Market Risk Consultancy

Market risk management consulting includes development and validation of risk measurement models, development of asset-liability management (ALM) framework, as well as the development of related policies and procedures.

Gap Analysis

Diagnostic review of operational risk management practices as compared to industry best practices and regulatory guidelines

Policy & Procedure

- Design and implement best-practices-based market risk management framework

- Treasury process reviews and process reengineering

- Preparation of market risk management and ALM policies

Model Validation

Validation of bank's internal models and other qualitative requirements

Measurement

Development of value-at-risk methodology

Asset Liability Management

- ALM monitoring and reporting framework

- Liquidity and interest rate risk measurement and management framework

- Framework for stress testing and funds transfer pricing

Asset-liability management (ALM) consulting covers:

- Diagnostic review

Review of organisation’s ALM-related processes, including risk management structure, underlying policies and procedures, and risk measurement and reporting frameworks.

- Risk assessment & measurement

Assessing extent of liquidity risk, taking into account gap reports, liquidity coverage ratio, net stable funding ratio and funding portfolio mix.

- Stress testing

Includes scenario analysis and sensitivity testing to assess impact of macro-economic and institution-specific stress scenarios on liquidity and interest rate.

- Risk control & monitoring

A limit management framework is designed, taking into account risk appetite and tolerance levels, as well as underlying and prospective portfolio mix.

- Risk-based decision-making

Mainly is in the form of funds-transfer-pricing-related consulting, including methodology. In addition, the plan for capital allocation, taking into account the liquidity and interest rate risk impact, is defined.

Valuation

- Valuation of derivatives

- Valuation of other market instruments

- Treasury performance assessment and monitoring framework

MarketRisk Rating Value at Risk Model Development

- Assessment of internal and external data (including proxy data elements) used in the model to ensure completeness

- Analysis of model assumptions

- Analysis of mathematical calculations and underlying risk factors

- Back-testing of data (past one year) at varying confidence intervals and sub-portfolios

- Conducting tests on VaR model, based on hypothetical portfolios

- Validation of model vis-à-vis benchmark/industry standard models

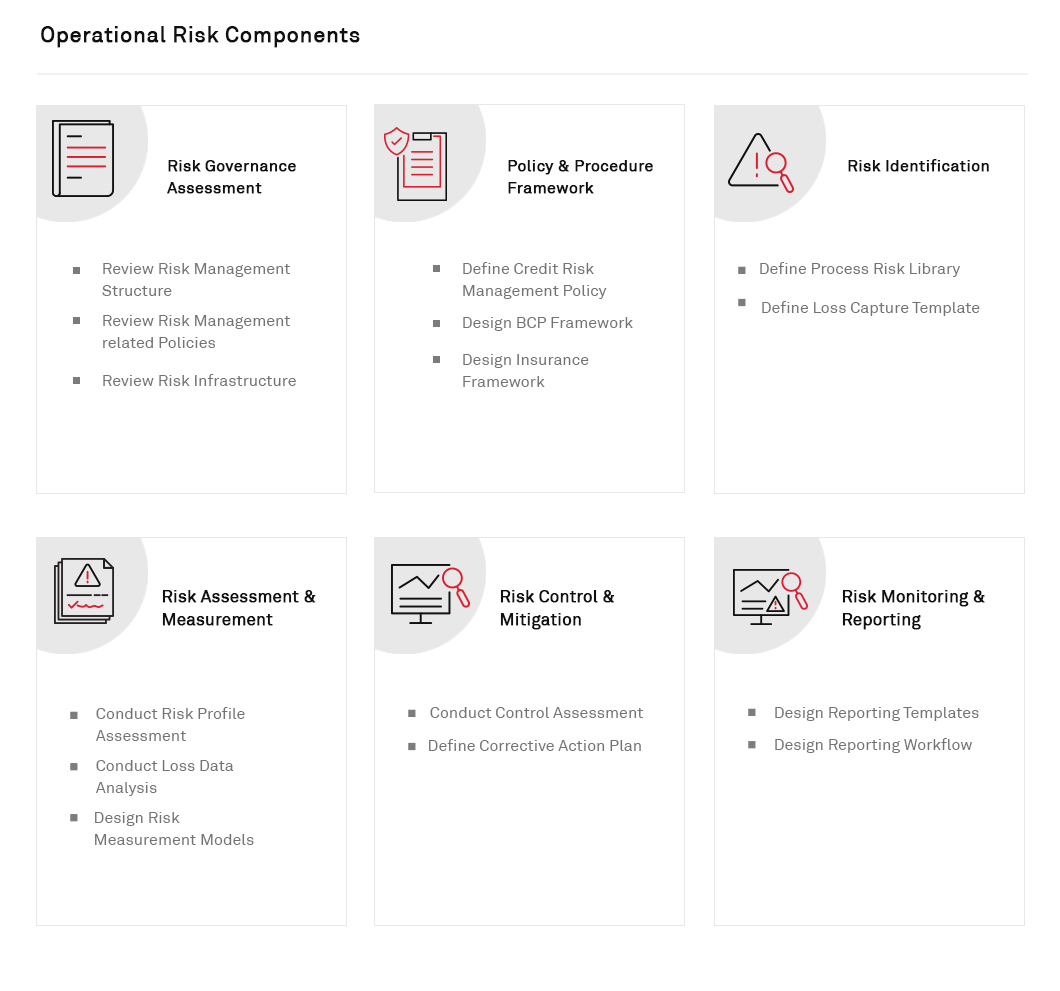

Operational Risk Consultancy

CRISIL Risk Solutions reviews, recommends and designs operational risk management frameworks.

Gap Analysis

- Diagnostic review of operational risk management practices as compared to industry best practices and regulatory guidelines.

Policy & Procedure

- Analysis of key business processes, development of workflow charts, identification/grading of possible operational risk areas

- Assess and mitigate operational risk

- Design control processes to assist in risk mitigation/minimisation

Risk Control Self-Assessment (RCSA)

- Design process-risk-control library to assist risk control self-assessment (RCSA)

- Design framework and template for RCSA

Key Risk Indicators (KRI)

- Design process flow and library for key risk indicators (KRI)

- Design KRI monitoring framework

Loss Data Management (LDM)

- Design framework to measure operational risk

- Design processes to analyse operational loss databases

- Design framework for loss data management

Model Validation

- Validate bank's internal models, etc to ensure compliance with advanced measurement approach

Operational Risk Consulting develops value-at-risk (VaR) models for operational risk measurement. It entails:

- Loss data collection across Basel business lines and loss event categories

- Loss data modeling

- Conduct "goodness of fit" test to assess strength of distribution

- Conduct simulation analysis

- Estimate operational loss VaR

- Back-testing to assess operational loss of VaR as against actual loss

- Operational risk capital charge estimation

- Estimate unexpected loss

- Scale-up factor, based on results of RCSA and KRI

- Value-at-risk model validation process includes:

- Assessment of internal and external data (including proxy data elements) used in the model to ensure completeness

- Analysis of model assumptions

- Analysis of mathematical calculation and underlying risk factors

- Back-testing of existing data

- Testing VaR model based on hypothetical portfolios

- Validation of model vis-a-vis benchmark/industry standard

- Assessment of reporting to senior management as regards

- Assessment of internal and external data (including proxy data elements) used in the model to ensure completeness

- Analysis of model assumptions

- Analysis of mathematical calculation and underlying risk factors

- Back-testing of existing data

- Testing VaR model based on hypothetical portfolios

- Validation of model vis-a-vis benchmark/industry standard

- Assessment of reporting to senior management as regards

Questions?

For any risk solution related queries, please contact:

+91 22 33428266

sales.risksolutions@crisil.com