RISE Roundtable: Default pooling consortium for low-default portfolio models

Summary

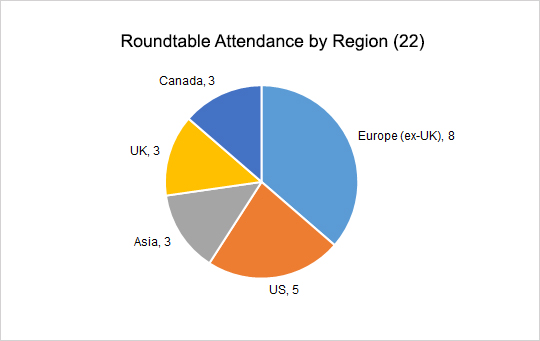

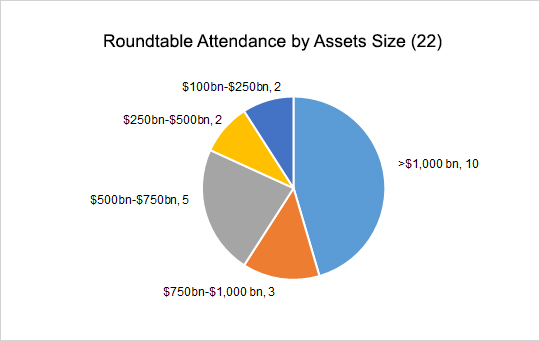

RISE hosted a virtual cross-bank roundtable to discuss the challenges faced by banks during both, development and validation of internal ratings/PD models for low-default portfolios. The session was attended by 38 senior credit modelling professionals from 22 banks of various domiciles and asset sizes.

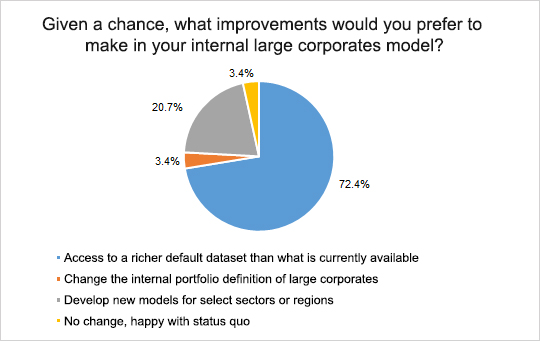

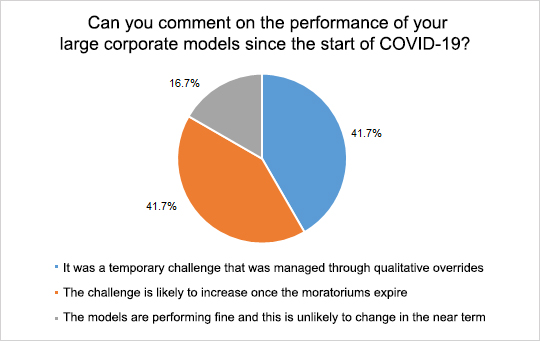

Most banks acknowledged the challenges faced in their low default portfolios, and that they mainly stem from the inadequacy of internal defaults. Furthermore, more than 80% of the banks said that their model outcomes were challenged since the start of the COVID-19 crisis, and half of this group felt that it may get even more challenging ahead once the moratorium period comes to an end. This hints at a possible need for re-visiting models, especially for those banks where such models have been developed many years ago. Furthermore, TRIM and Basel III reform are other driving factors for model re-development.

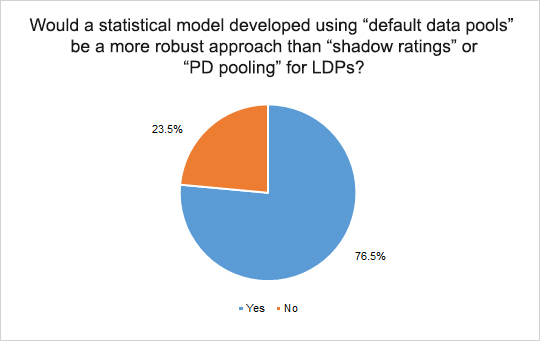

RISE presented the specifics of its LDP data pooling consortium solution, which pools data on both, defaulted and performing obligors, with the objective of enabling banks to carry out robust testing or even re-development of their models. The solution focuses on two specific portfolios – a) banks, and b) large corporates. These two portfolios are where the scarcity of defaults in most pronounced and also the likelihood of a creating rich dataset from pooling is high. RISE demonstrated how the solution works and that it is designed to meet regulatory requirements across of all major jurisdictions. In a closing spot poll, more than 75% of the banks agreed that a logistic regression model developed using ‘default pools’ would be more robust than current industry practices of shadow ratings based on a) either external agency ratings, or b) PD pooling consortiums.

The RISE LDP data consortium already includes multiple G-SIBs that have contributed their data to the pool. We are now looking to accelerate the consortium membership across global and regional banks. If you are a banker who is interested in learning more about the consortium, please contact us at rise@crisil.com.

You can also read our white paper on the benefits of data pooling here.

Subscribe for Crisil events