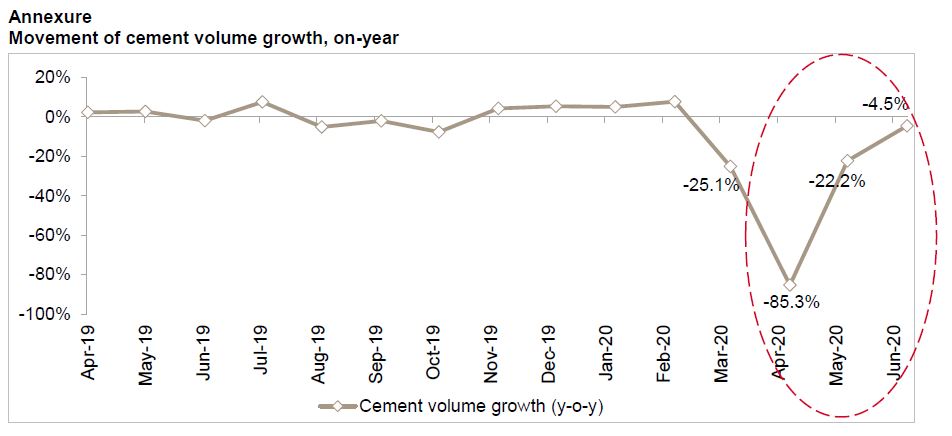

A surge in demand from rural and affordable housing segments will help contain the on-year drop in cement sales volume to 12-14% this fiscal, compared with an average annual growth of ~6% during the last three fiscals. That would mark a V-shaped recovery from a sharp contraction of 85% seen in April to an estimated 7-10% growth by the fourth quarter, an analysis of 19 cement makers comprising ~73% of the industry’s installed capacity shows.

Rural demand will ride on higher agricultural income and a sharp rise in spending under the Mahatma Gandhi National Rural Employment Guarantee Act to engage migrant workers who have returned home following the Covid-19 pandemic. Also, given expectations of another normal monsoon this year, a third consecutive season of healthy agriculture income looms.

Says Isha Chaudhary, Director, CRISIL Research, “The pandemic-led lockdown resulted in a near washout of cement sales volume in April, but rural demand vertically yanked up recovery in May and June. Demand recovery, however, has not been uniform across regions and bears a likeness to the intensity of the pandemic – East and Central regions are more resilient, while West and South are more impacted.”

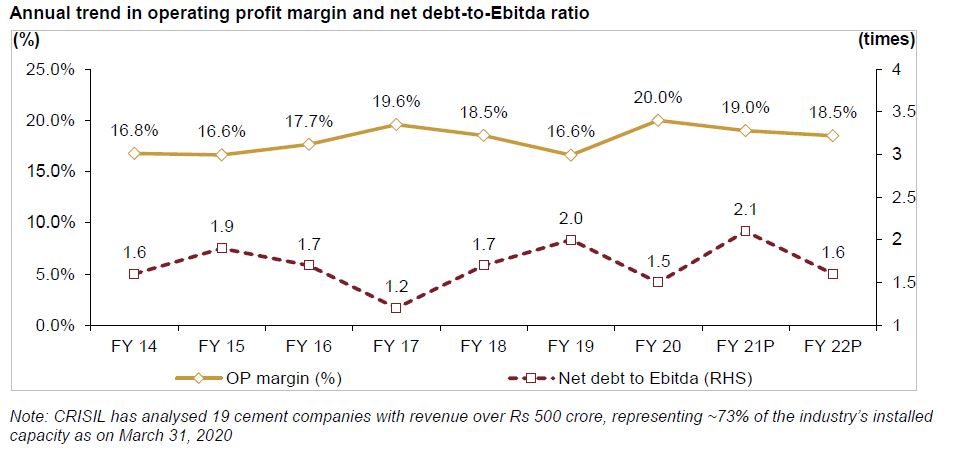

Lower volume will result in a 50-100 basis points (bps) moderation in earnings before interest, taxes, depreciation and amortisation (Ebitda), or the operating profit margin, to around 19% this fiscal (refer to charts in annexure). This would be despite some support from healthy realisation and lower prices of pet coke, which is a key input.

To be sure, operating profitability had touched a seven-year high of around 20% last fiscal, helped by healthy growth in realisation and benign input costs. Prices are expected to hold this fiscal, too, as seen during the first quarter.

Despite the volume contraction and lower cash accrual, credit profiles of cement makers won’t be impacted.

Says Nitesh Jain, Director, CRISIL Ratings, “The credit profiles of cement makers are resilient because of healthy balance sheets, as indicated by a comfortable net debt-to-Ebitda ratio of around 2.0 times this fiscal. In addition, adequate liquidity maintained by most cement makers will afford a bolster. Lower capital expenditure, and mergers and acquisition activity will also be supportive.”

Cement makers had liquidity of Rs 23,000 crore as on March 31, 2020, which is more than their debt repayment due this fiscal.

To maintain liquidity, cement companies are likely to cut down capital expenditure by 30-40% this fiscal. Also, while cement companies have been acquisitive in recent past, the sector is now fairly consolidated and large sized M&A deals are unlikely in the near term.

The dynamics could change as things are evolving continuously. The rise in Covid-19 cases in the hinterland and intermittent lockdowns pose downside risks to our assumptions, while on the upside, the risks include a sooner-than-expected revival of industrial capex and government spending on infrastructure.

Mumbai

Mumbai