Nearly two-thirds of the companies rated by CRISIL would be eligible for one-time debt restructuring based on the parameters proposed by the K V Kamath Committee set up by the Reserve Bank of India (RBI). The RBI had, in a circular on August 6, 2020, announced the constitution of the committee to draw up sector-specific eligibility parameters for companies, which would enable restructuring of their bank loans.

The committee submitted its recommendations1 for 26 sectors. For others, it said lenders should make their own internal assessments, but mandated that the current ratio and debt service coverage ratio (DSCR) should be above 1 time and average DSCR above 1.2 times. While this will help identify eligible companies, the decision to restructure will be a function of company performance. The circular also said companies with outstanding debt of over Rs 100 crore will need a credit rating threshold. That means company-specific parameters and credit rating will play a material role in the final restructuring decision.

CRISIL studied its rated portfolio of more than 8,500 companies after sorting them by rating, sector and moratorium availed. The broad-level assessment is based on financial projections and excludes small and medium enterprises (SMEs) and financial sector companies (please refer to annexure for methodology)

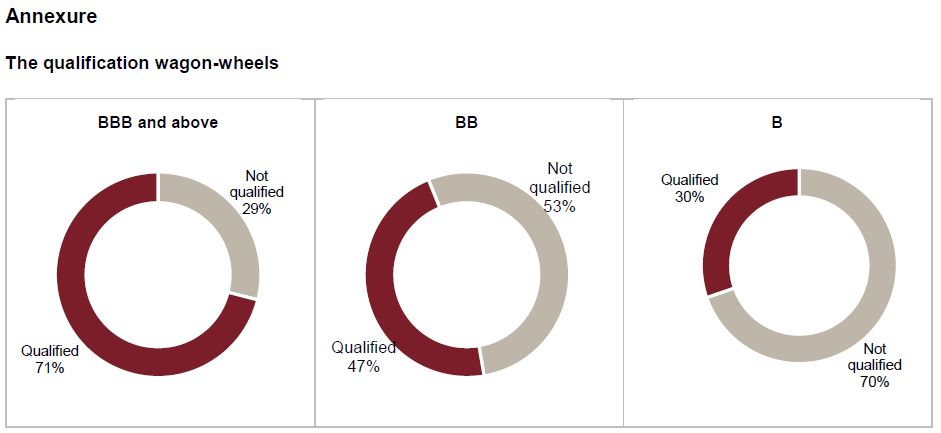

Says Subodh Rai, Senior Director, CRISIL Ratings “Three out of four investment-grade companies (rated CRISIL BBB- or higher) and one out of two in the BB rating category qualify for restructuring of bank loans. However, in the CRISIL B category, only one in three qualify because companies here tend to have relatively weak debt protection metrics. At an aggregate CRISIL portfolio level, two out of three companies were found eligible for restructuring.”

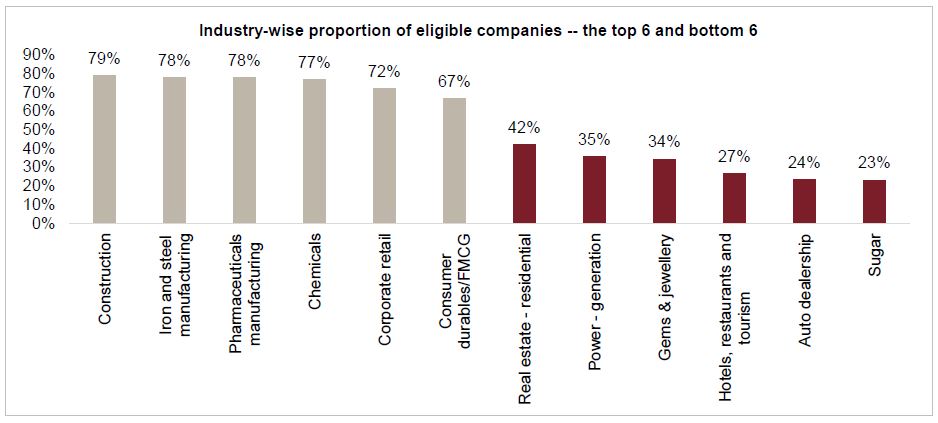

While the parameters support debt restructuring across rating categories, the study indicated that companies in the resilient^ sectors stand to benefit more. Three out of four rated ones in the resilient sectors such as construction, chemicals, pharmaceuticals, iron and steel manufacturing, corporate retail, and consumer durables/FMCG will qualify for restructuring.

In the less-resilient sectors such as auto dealerships, gems and jewellery, hotels, restaurants and tourism, power generation, and real estate, opportunities for debt restructuring could be a little lower as they can take longer to recover to pre-pandemic business levels. Here, only one in three companies could be eligible for restructuring.

Restructuring will also be available to a large number of companies that opted for the moratorium. Every second company in the CRISIL-rated portfolio that did so** will qualify for restructuring.

While the qualification parameters have been defined in the framework laid out by the committee, lenders are also expected to use their discretion when assessing each restructuring proposal.

Says Rahul Guha, Director, CRISIL Ratings “The situation is still evolving and actual number of eligible companies could increase in case of favourable developments such as faster than expected turnaround of the economy, banks choosing to convert interest charges to funded interest term loan or exploring other innovative ways of restructuring or promoters bringing in capital. A final picture on how many companies have qualified for restructuring will only emerge over the next 3-4 months.”

CRISIL will factor in the impact of debt restructuring on its rated credits as and when the process is initiated and will take a view on a case-to-case basis after factoring in the standalone credit risk profile of the company and timeliness and terms of the restructuring of debt.

1 These parameters include TOL/ATNW (total outside liabilities/adjusted tangible networth), Debt/EBIDTA (debt/earnings before interest, taxation, depreciation and amortisation, Current ratio (current assets/current liabilities), DSCR = EBIDTA/(interest + principal repayment for the year)) and ADSCR (average DSCR)

^ Sectoral resilience is the ability of a sector to sustain the revenue impact of Covid-19 and bounce back to full production after the pandemic peters out.

** A detailed analysis was carried in CRISIL’s press release titled, ‘75% of companies availing of moratorium are sub-investment grades’ dated August 31, 2020

Mumbai

Mumbai