Ex-gratia payment of interest-on-interest1 by banks and non-banking finance companies (NBFCs2) for the moratorium period (between March 1, 2020, and August 31, 2020) would tantamount to a ~Rs 7,500 crore benefit for eligible borrowers – with the tab being picked up by the government, CRISIL’s analysis based on guidelines for such payments announced by the Ministry of Finance on Friday shows.

The benefit will be extended to borrowers with outstanding loans (standard as on February 29, 2020) of less than Rs 2 crore under select categories3, irrespective of whether the moratorium was availed of or not. Such loans account for more than 40% of systemic credit and 75% of borrowers.

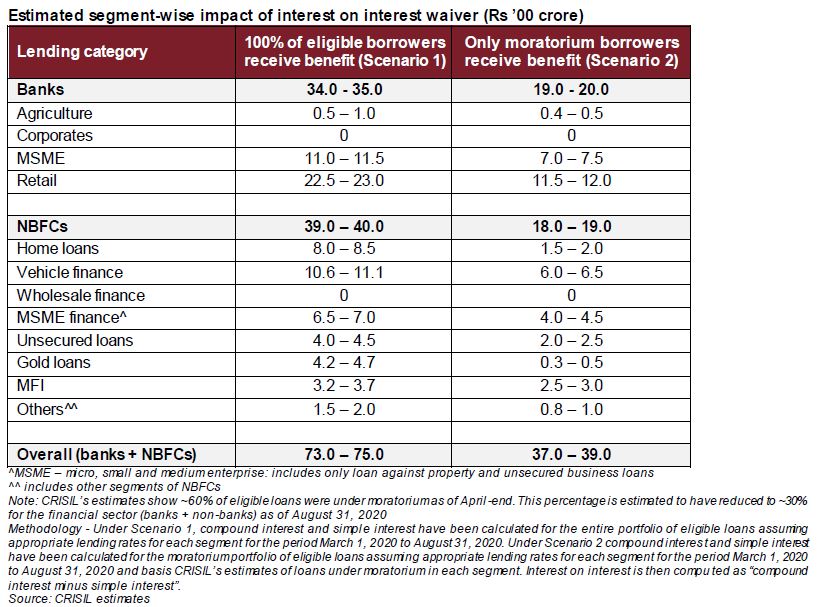

The cost to exchequer would have halved if waiver was allowed only where moratorium was availed of.

Also, to ensure effective and timely implementation, the government has asked lenders to credit the amount to eligible borrowers latest by November 05, 2020. This will be the difference between compound interest and simple interest over six months (March 1, 2020 to August 31, 2020). While lenders have to apply for reimbursement by December 15, 2020, the timelines for receipt of funds from the government are yet to be notified.

Says Krishnan Sitaraman, Senior Director, CRISIL Ratings, “CRISIL’s analysis shows a complete interest waiver (including interest on interest) for eligible loans up to Rs 2 crore would have meant a staggering ~Rs 1.5 lakh crore impact. This could have posed significant challenges for the government as well as the financial sector. Waiver of only interest-on-interest will have a much milder and manageable impact.”

With the government expected to bear the cost of waiver on small-borrower loans, the potential burden on lenders – already facing profitability pressure and asset-quality challenges because of the Covid-19 pandemic and challenging macroeconomic environment – has eased.

From a borrower’s perspective, the benefit would be relatively higher for those who had availed of higher-yielding loans. Consequently, borrowers of unsecured, micro and gold loans will benefit more than those who had taken home loans.

Says Malvika Bhotika, Associate Director, CRISIL Ratings, “Extending the benefit to all eligible borrowers irrespective of whether they have availed of moratorium or not, will assuage concerns over unfair treatment that borrowers not availing of moratorium could have otherwise harboured.”

While the waiver will offer a modicum of relief in terms of cash flows, repayment discipline among borrowers after the moratorium ended – and thus medium-term delinquencies at banks and NBFCs – will bear watching.

1 Defined as compound interest minus simple interest

2 NBFCs including housing finance companies, but excluding government-owned NBFCs

3 Loan segments eligible for waiver are MSME, education, housing, consumer durables, credit card, automobile, personal, professional, and consumption

Annexure

Mumbai

Mumbai