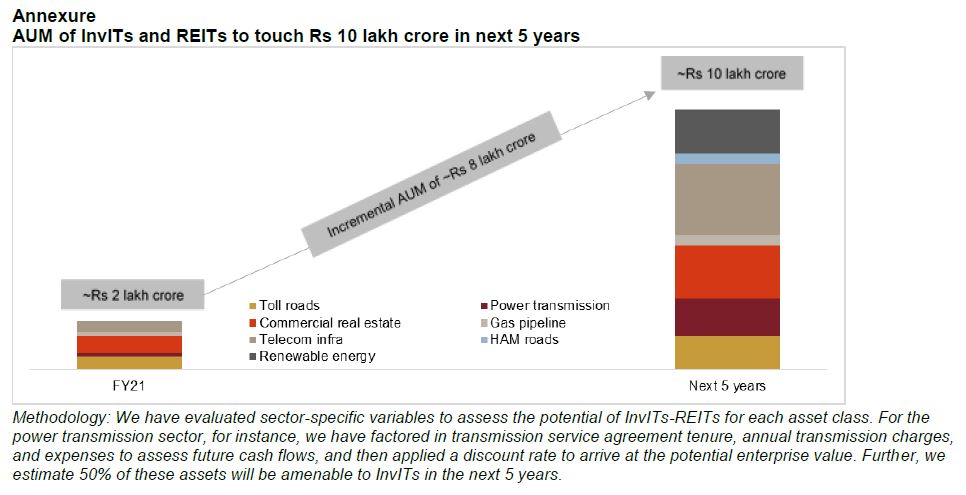

Infrastructure investment trusts (InvITs) and real estate investment trusts (REITs) are gaining currency in India, following the footsteps of the developed world. A CRISIL Ratings analysis shows these instruments can potentially raise up to Rs 8 lakh crore of capital for India’s infrastructure buildout over the next five fiscals.

A deeper debt market where investors can discern risks and returns across infrastructure asset classes, and stable regulations will be critical to achieving this goal.

A government task force has estimated that Rs 111 lakh crore1 of investments are required in infrastructure through fiscal 2025 – or twice what was spent in the past five fiscals. That’s a humungous investment need, and cannot be met by the government and traditional infrastructure-financing channels alone. Thus, alternative channels need to be pressed into service.

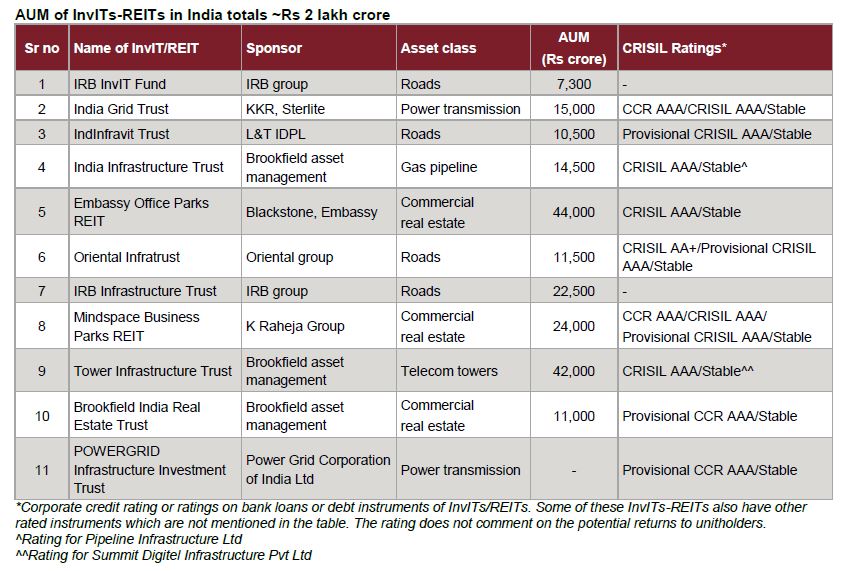

InvITs and REITs can play a significant role here. Their combined assets under management (AUM) have logged a whopping 42% compound annual growth rate (CAGR) since the launch of the first InvIT in fiscal 2018 to ~Rs 2 lakh crore now (see annexure).

Says Manish Gupta, Senior Director, CRISIL Ratings Ltd, “Investments under InvITs and REITs can grow by another Rs 8 lakh crore over the next five fiscals, driven by an enabling regulatory framework, ample availability of operational infrastructure2 and real estate assets, and increasing appetite from global and domestic investors looking to invest in high-yield assets.”

There is also support from regulation, such as cap on leverage and allowing investments in operational assets. Regulations also stipulate a AAA rating threshold for listed InvITs if their debt-to-AUM ratio exceeds 49%, among other conditions, which reduces the credit risk. Further, mandatory distribution of surplus cash also enhances investor confidence.

Currently, there are 11 InvITs and REITs in India. Credit ratings on ten of these demonstrate the highest safety level (AAA) for three reasons: low debt, combined debt-to-AUM ratio of less than 35%, and over 90% of AUM deployed in operational assets.

Lower leverage in most situations is driven by regulations, but this is set to change. Recent rules afford setting up of an unlisted private InvIT sans any cap on leverage or ratings, or curbs on investments in operational assets. While this could raise credit risks by some extent, it may still support holistic market development. Such InvITs are increasingly generating investor interest given the flexibilities offered and the opportunity to balance the interests of lenders and investors.

Globally, even lower-rated InvITs and REITs are accepted. For instance, 12% of S&P Global’s rated REITs in the US are in the ‘BB’ category, while 77% are in the ‘BBB’ category. To be sure, these ratings are on their bank loans, or debt instruments, indicating the likelihood of timely payment of the obligation under the rated instrument – and not a comment on the potential returns to unitholders, which are anyway subservient to debt.

As the market expands and regulations open up, the landscape will change, necessitating sharper differentiation in the credit and operating risks of InvITs and REITs.

Says Nitesh Jain, Director, CRISIL Ratings Ltd, “Lenders and unitholders need to differentiate the varying nature of operating risks of underlying asset classes. For instance, the cash-flow stability of a power transmission project is higher than that of a solar power project. Typically, a power transmission project’s revenue is linked to the availability of lines and not the actual transmission, whereas a solar power project’s revenue is linked to the power generated. Therefore, a power transmission project carries low operating risk and can sustain higher debt.”

InvITs and REITs have the potential to emerge as an important tool to address India’s gigantic infra financing needs. Debt market depth, greater understanding of operating and credit risks among investors and unitholders, and stable regulations are essential to achieve projected growth.

1 Source: Union Budget 2020

2 Across sectors such as roads, renewable energy, power transmission, gas transportation, telecom infrastructure, etc.

Mumbai

Mumbai