The tyre sector is one of few, whose operating profits are expected to register growth this year, surpassing pre-covid levels, despite lower volume. Higher realisations and benign input prices will help offset the impact of 4-6% volume decline, and enable a 6-8% growth in operating profits for tyre manufacturers in fiscal 2021.

That, along with phased implementation of capital expenditure plans, will ensure stable credit outlook for tyre manufacturers. This is based on CRISIL Ratings’ analysis of India’s top six tyre manufacturers, accounting for ~80% of the Rs 60,000 crore automobile tyre sector revenue.

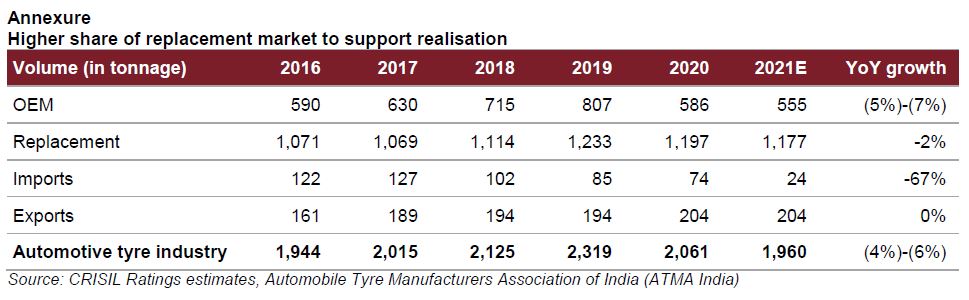

The sector derives 28% of its volume (in tonnage terms) from original equipment manufacturers (OEMs), 58% from the replacement market, 10% from exports, and the rest from imports.

Tyre offtake by OEMs is seen skidding ~5-7% this fiscal primarily on account of a sharp decline in demand from the commercial vehicle (CV) segment. This would get partially offset by robust demand from the tractor segment. Replacement demand is seen slipping just 2% because of support from pent-up demand from existing CVs, uptick in freight movement and improving economic activity (see table in annexure).

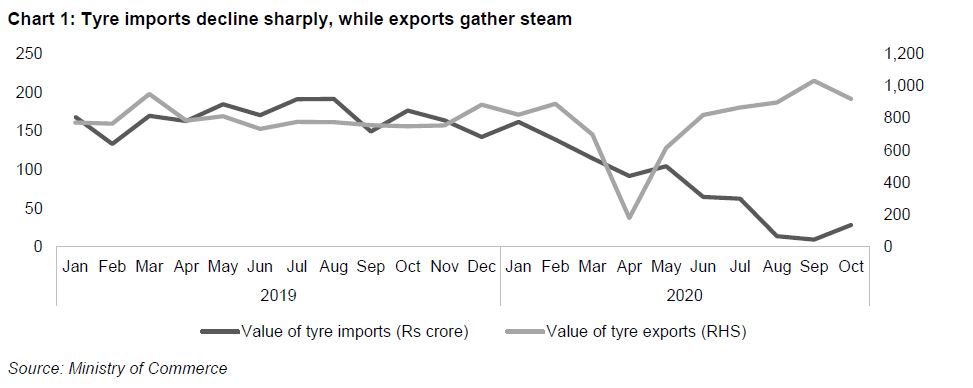

Exports volume is expected to sustain because of increasing replacement demand in the overseas markets for tractor and CV tyres, which account for 90% of tyre exports (see chart in annexure). Hence, the tyre sector is likely to log only a moderate volume decline of 4-6%.

Says Anuj Sethi, Senior Director, CRISIL Ratings Ltd, “Improved realisations on account of increased share of replacement demand (to 60% from 58% in fiscal 2020) and exports, which command better prices, will drive the increase in operating profits of tyre manufacturers this fiscal. Tyre makers have also increased prices in the domestic market after imports were placed on restricted list in June 2020. The average realisation per tonne of tyres is expected to increase 4-5% this fiscal.”

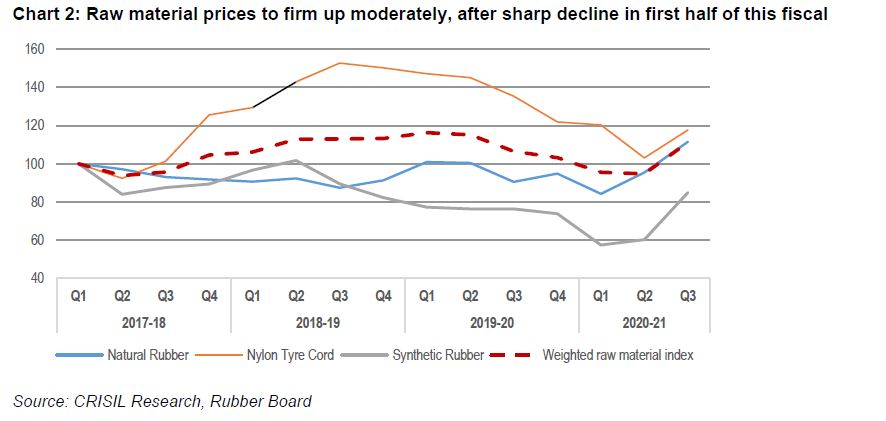

Input costs1 also fell 18% in the first half of the fiscal given the subdued global demand for automobiles and softer crude prices (crude derivatives account for about 40% of raw material requirement).

Though prices are expected to firm up moderately in the second half on account of lower global production of natural rubber and increase in crude prices, overall input cost will still be lower this fiscal (see chart in annexure).

Higher realisations and lower input cost will improve the average operating margin of tyre manufacturers by 100-120 basis points to about 14% this fiscal, leading to an average 6-8% increase in operating profit.

Pick-up in OEM demand across vehicle segments and higher replacement demand for CV tyres following recovery in economic activity will drive domestic volume up next fiscal. Operating margins of tyre manufacturers will sustain at 13-14%, driven by higher volume and continued pricing flexibility, supported by favourable import policies.

Added to this, capital expenditure (capex) is expected to remain modest this fiscal. As against the planned capex of about Rs 18,000 crore over fiscals 2021-23 (compared with Rs 18,500 crore over fiscals 2018-20), capex of less than Rs 1000 crore were incurred during the first half of this fiscal, and we expect players will exercise caution in stepping up capacity, given sufficient available capacity and uncertainty around the pandemic.

Says Rajeswari Karthigeyan, Associate Director, CRISIL Ratings Ltd, “The credit outlook for tyre manufacturers should remain stable over the medium term, supported by likely phasing out of capex plans and steady accruals. Gearing and interest coverage for the sample set are expected at around 0.5 time and 6-7 times, respectively, over the medium term, similar to the levels seen in fiscal 2020.”

That said, the extent of demand recovery, especially for CVs, and change in regulations regarding tyre imports will be key monitorables. Exports could benefit further if the US implements the proposed anti-dumping duty on select Asian countries2 (which constitute 30% of US tyre imports).

1 Raw materials include natural and synthetic rubber, nylon tyre cord, and carbon black, which account for 90% of tyre-making inputs

2 The US is considering anti-dumping duties on Korea, Thailand, Taiwan and Vietnam; countervailing duties were proposed on Vietnam in November 2020.

Mumbai

Mumbai