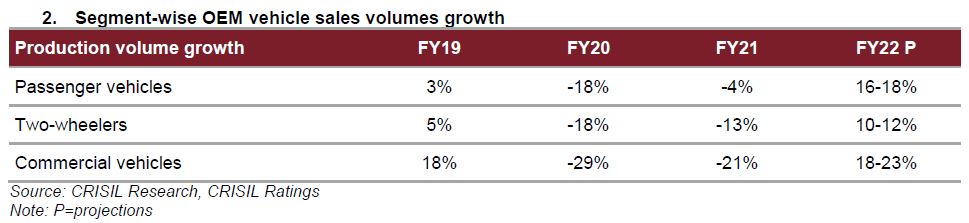

Passenger vehicles (PV) dealers are expected to lead a recovery amongst all automobile dealers sub segments with 20-22% revenue growth this fiscal to almost reach pre-pandemic revenue levels of fiscal 2020. Comparatively, due to slower recovery, two-wheeler (2W) dealers will take a year or so longer to reach pre-pandemic sale levels. Revenues for commercial vehicles (CV) dealers will remain below pre-pandemic levels this fiscal despite higher revenue growth due to a low base created by sharp fall in last two fiscals.

The pace of recovery could have been swifter, but for the second wave of Covid-19 infections, which led to partial shutdown of dealers’ showrooms in the first quarter of fiscal 2021. Even so, automobile dealers’ overall revenues will still likely grow at ~20% on a low base, also supported by 4-6% price hikes across vehicle segments.

Cash flows are expected to gradually recover, and along with controlled channel inventory and limited increase in debt, lend stability to credit profiles this fiscal. A study of 191 automobile dealers rated by CRISIL Ratings indicates as much.

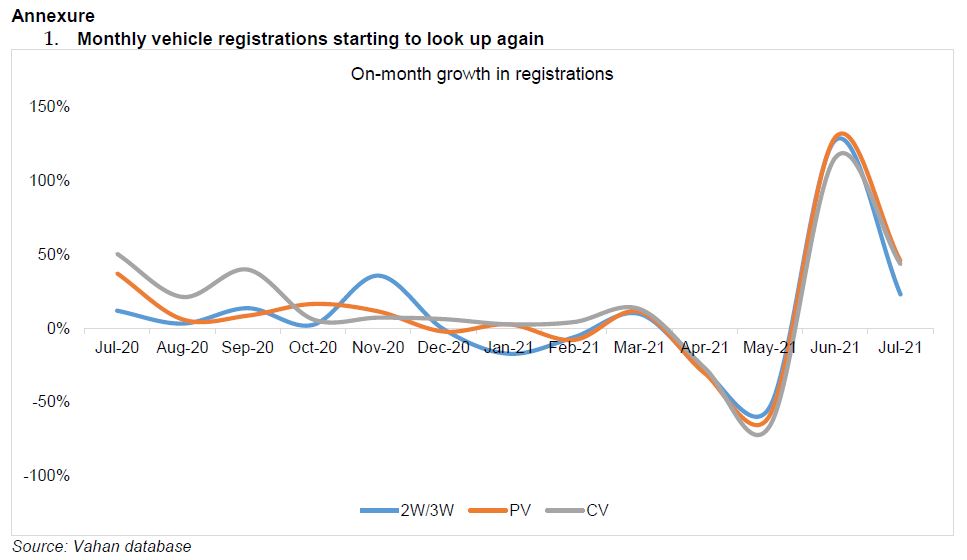

Automotive retail registrations plunged in April and May (as reflected in annexure 1), respectively, due to localised lockdowns and temporary dealers’ showroom closures amid the intense second wave. June saw a sharp recovery, on a low base and with easing of curbs, the recovery is seen continuing in July. More so, because the restrictions were mainly imposed in key states such as Maharashtra, Uttar Pradesh, Tamil Nadu, Karnataka and Rajasthan, which account for a big chunk (43-45%) of the total retail automotive retail sales in India.

From mid-June onwards, a reduction in active Covid-19 case load and increasing pace of vaccination will drive recovery in automobile demand (refer annexure 2) this fiscal.

Says Anuj Sethi, Senior Director, CRISIL Ratings, “PV dealers seem to be recovering faster compared with other categories, riding on higher pent-up demand and preference for personal mobility, especially in urban and semi-urban areas. Slower demand from pandemic-hit hinterland, increased spend on health and prices hikes are likely to impact the pace of recovery in two-wheelers (2Ws) dealers. As a result, PV dealers’ revenues will grow at 20-22%, well over 15-16% revenue growth for 2W dealers. CV dealers, though, will see healthy revenue growth of 28-30% this fiscal on a low base, but will remain below pre-pandemic levels given sharp fall in the previous two fiscals.”

The intermittent lockdowns during the first quarter of this fiscal is likely to result in only ~50 basis points recovery in operating profitability to 2.5-3% this fiscal, which is still below the pre-pandemic level of 3-4%. This is because service and spare sales (10-12% of revenues but 25% of operating profits of automotive dealers) are also witnessing muted recovery.

While business performance was severely dented last fiscal, dealers availed of moratorium and emergency credit facilities offered by banks and support from captive finance arms of original equipment manufacturers (OEMs) as well as OEMs themselves through inventory funding limits and higher credit period, respectively, to tide over liquidity pressures. This year too, similar support is expected to continue for dealers from OEMs or their captive finance arms until sales recover completely.

Says Gautam Shahi, Director, CRISIL Ratings, “Controlled inventory levels at auto dealers’ end due to lower dispatches from OEMs, and recovery in margin will ensure limited increase in short-term debt this fiscal. However, slower demand recovery for 2W and CV dealers to pre-pandemic levels will result in relatively gradual improvement in debt metrics for them compared to PV dealers. Overall for auto dealers, key debt metrics such as interest coverage and gearing are seen improving to 2.2-2.4 times and 1.4 times in fiscal 2022, compared to 1.9 times and ~1.5 times, respectively, for last fiscal.”

Sustenance of recovery in demand across segments, and normal monsoon will remain monitorables.

Mumbai

Mumbai