Formerly known as Market Intelligence & Analytics

Formerly known as Market Intelligence & Analytics

Risk Consulting

We help financial institutions develop and validate risk models, design scorecards and calculate risk parameters.

Risk Models and Framework Services

Framework

Policy & Procedure

Gap Analysis

Model Validation

Model Development

Parameter Estimation

Credit VaR Estimation

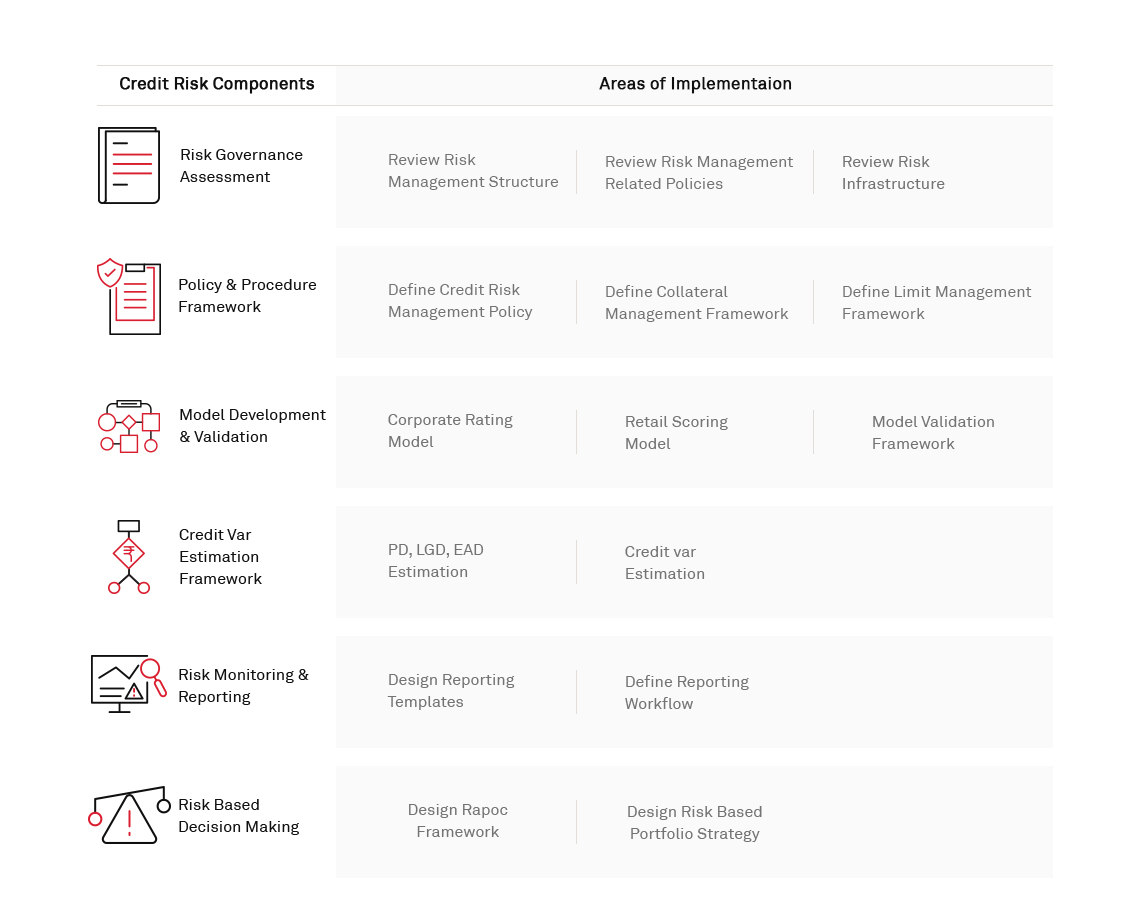

Credit Risk Consultancy Services

Framework

Gap Analysis

Policy & Procedure

Model Development

Model Validation

Parameter Estimation

Credit VaR Estimation

Market Risk Consultancy Services

Market risk management consulting includes development and validation of risk measurement models, development of asset-liability management (ALM) framework, as well as the development of related policies and procedures.

Framework

Gap Analysis

Policy & Procedure

Model Validation

Measurement

Asset Liability Management

Valuation

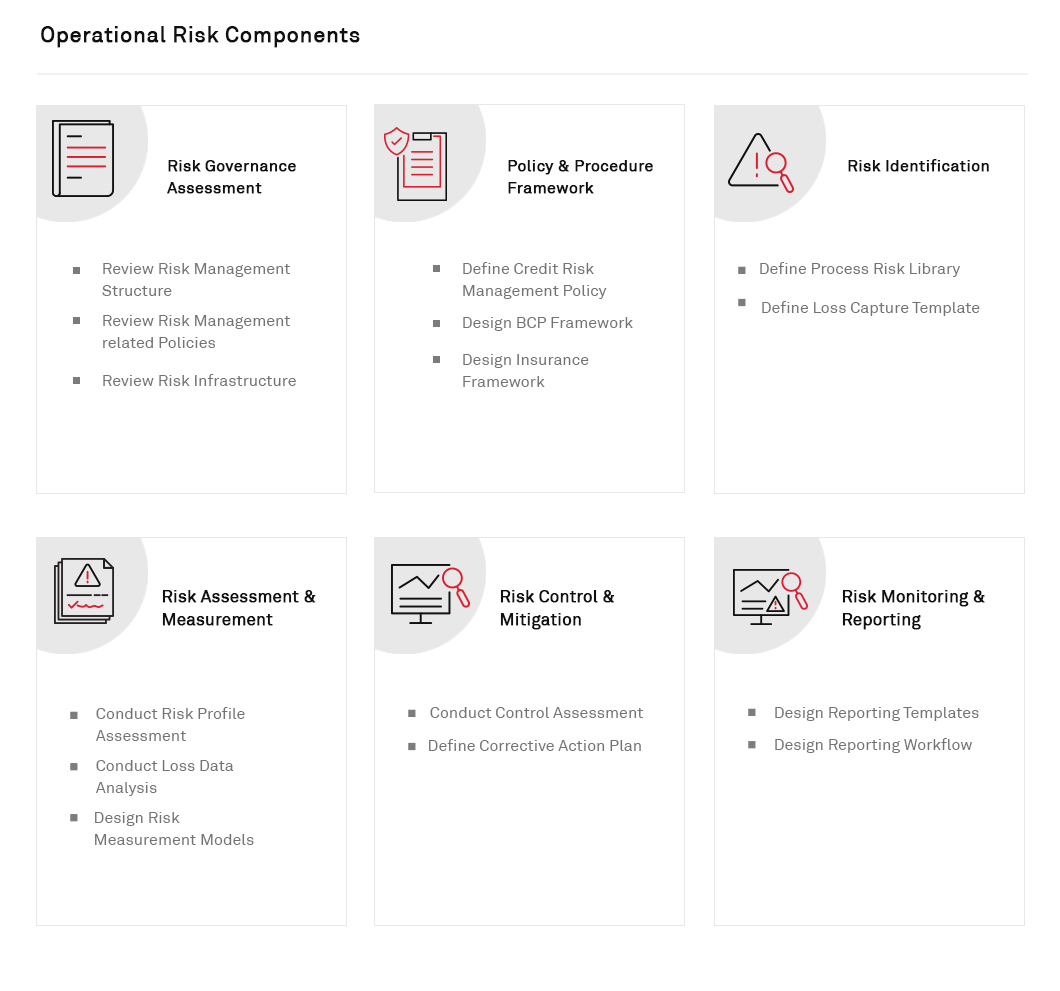

Operational Risk Consultancy

Crisil Risk Solutions reviews, recommends and designs operational risk management frameworks.

Framework

Gap Analysis

Policy & Procedure

Risk Control Self-Assessment (RCSA)

Key Risk Indicators (KRI)

Loss Data Management (LDM)

Model Validation