Page 116 - Index

P. 116

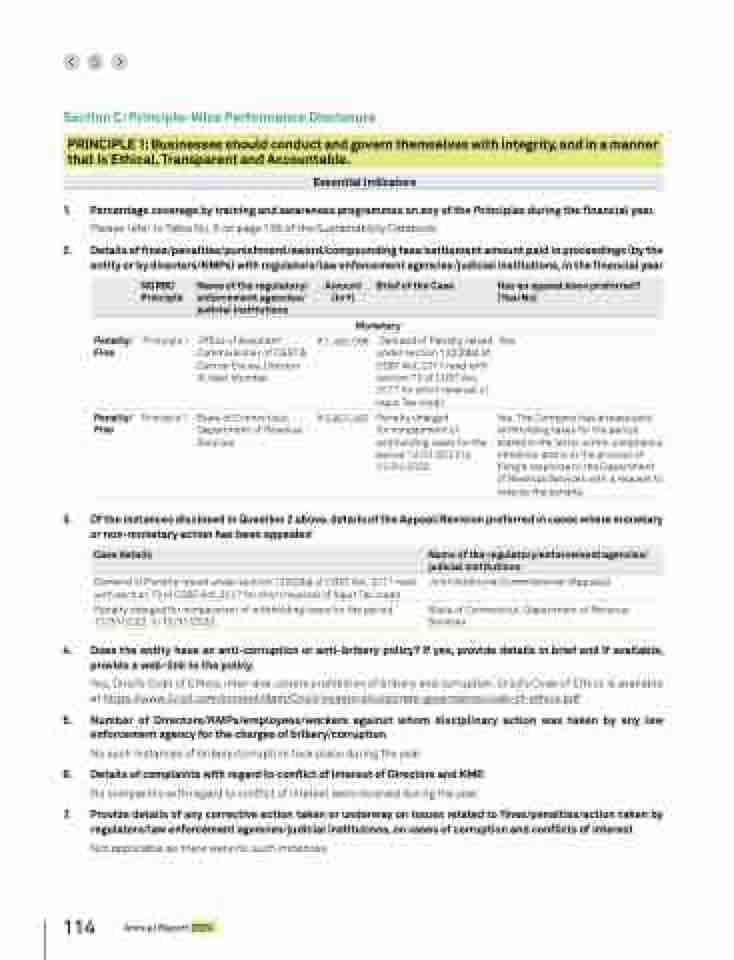

Section C: Principle-Wise Performance Disclosure

PRINCIPLE 1: Businesses should conduct and govern themselves with integrity, and in a manner

that is Ethical, Transparent and Accountable.

Essential Indicators

1. 2. Percentage coverage by training and awareness programmes on any of the Principles during the financial year.

Please refer to Table No. 6 on page 135 of the Sustainability Databook

Details of fines/penalties/punishment/award/compounding fees/settlement amount paid in proceedings (by the

entity or by directors/KMPs) with regulators/law enforcement agencies/judicial institutions, in the financial year

NGRBC

Principle

Name of the regulatory/

enforcement agencies/

judicial institutions

Amount

(In J)

Brief of the Case Has an appeal been preferred?

(Yes/No)

Monetary

Penalty/

Fine

Principle 1 Office of Assistant

Commissioner of CGST &

Central Excise, Division

III, Navi Mumbai

C 1,460,066 Demand of Penalty raised

under section 122(2)(a) of

CGST Act, 2017 read with

section 73 of CGST Act,

2017 for short reversal of

Input Tax credit

Yes

Penalty/

Fine

Principle 1 State of Connecticut,

Department of Revenue

Services

C 5,857,487 Penalty charged

for nonpayment of

withholding taxes for the

period 12/31/2022 to

12/31/2023.

Yes. The Company has already paid

withholding taxes for the period

stated in the letter within compliance

timelines and is in the process of

filing a response to the Department

of Revenue Services with a request to

reverse the penalty.

3. Of the instances disclosed in Question 2 above, details of the Appeal/Revision preferred in cases where monetary

or non-monetary action has been appealed

Case details Name of the regulatory/enforcement agencies/

judicial institutions

Demand of Penalty raised under section 122(2)(a) of CGST Act, 2017 read

with section 73 of CGST Act, 2017 for short reversal of Input Tax credit

Joint/Additional Commissioner (Appeals)

Penalty charged for nonpayment of withholding taxes for the period

12/31/2022 to 12/31/2023.

State of Connecticut, Department of Revenue

Services

4. 5. 6. 7. Does the entity have an anti-corruption or anti-bribery policy? If yes, provide details in brief and if available,

provide a web-link to the policy.

Yes, Crisil’s Code of Ethics, inter-alia, covers prohibition of bribery and corruption. Crisil’s Code of Ethics is available

at https://www.Crisil.com/content/dam/Crisil/investors/corporate-governance/code-of-ethics.pdf

Number of Directors/KMPs/employees/workers against whom disciplinary action was taken by any law

enforcement agency for the charges of bribery/corruption

No such instances of bribery/corruption took place during the year.

Details of complaints with regard to conflict of interest of Directors and KMP.

No complaints with regard to conflict of interest were received during the year.

Provide details of any corrective action taken or underway on issues related to fines/penalties/action taken by

regulators/law enforcement agencies/judicial institutions, on cases of corruption and conflicts of interest

Not applicable as there were no such instances.

114 Annual Report 2024