Economy

CRISIL IndiaInsights

Nov - Dec 2019

Pain points aplenty

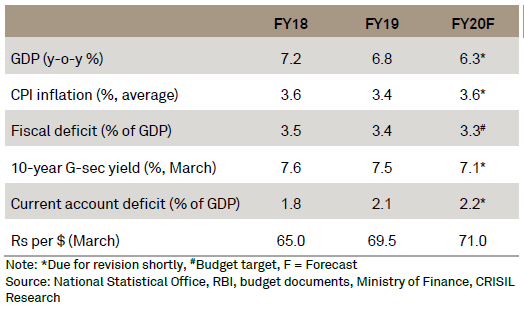

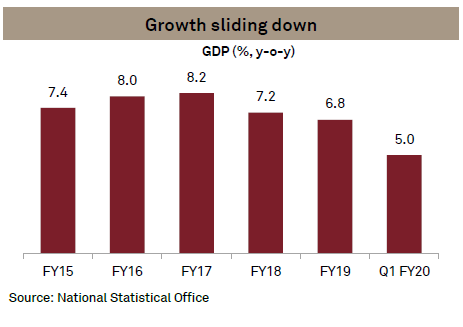

The Indian economy is going through a more-than-anticipated slowdown, as weakness in the real sector and stress in the financial sector are feeding into each other and spiralling down growth. That gross domestic product (GDP) growth in the second quarter this fiscal will print below the 5% logged in the first, appears certain now.

Key short-term indicators such as industrial production, exports, bank credit, tax collections, freight movement, electricity production, and credit, all point to weakening growth momentum. Although inflation spiked, core inflation fell sharply, confirming that demand is slipping. Slowing global growth, falling trade intensity, and uncertainties stemming from trade conflict are hurting, too. Interestingly, this slowdown is atypical, in the sense that it is accompanied by the cleaning-up of the financial sector – something that’s happening after almost 20 years. That has the potential to stretch the slowdown, particularly when the policy space to fire the economy in the short run is limited.

Monetary policy, too, has lost its bite. Despite a cumulative repo rate cut of 135 basis points (bps) by the Reserve Bank of India (RBI), lending rates have come down only 20-30 bps. With the slowing economy, the demand for credit has come down, but the risk aversion and weak sentiment mean the willingness to supply credit, too, has reduced. Amid the gloom and doom, the big picture for the medium run remains promising – with 7% per year growth over the medium run. We believe India’s transition from around 5% GDP growth in April-June quarter of 2019, to 7% over the next five years, will be complimented by steps that improve the quality of growth.

First, healthier corporate balance sheets and a stronger banking sector will underpin recovery. More importantly, the clean-up of the financial system has been accompanied by steps that will improve India’s credit culture. We are moving towards a system that not only improves the ability of the banks to recover their debts, but also, for the first time, instils in promoters the fear of losing their companies altogether. Second, reforms such as the Goods and Services Tax and the Insolvency & Bankruptcy Code are expected to improve allocation and efficiency of capital, and create possibilities of an efficiency-led spurt in growth, once streamlined.

All this, however, requires relentless implementation of reforms. The current slowdown provides the government the opportunity to use its abundant political capital to push for hard reforms to make labour laws flexible, make acquisition of land easier, and improve the ease of doing business further.

Analytica