Economy

Uphill trek

Executive summary

With the Indian economy caught in crosswinds, we now expect gross domestic product (GDP) to grow 6.9% this fiscal, or 20 basis points lower than what we had envisaged earlier.

The revision factors in a triangulation of downside risks: inadequate monsoon, slowing global growth, and sluggish high-frequency data for the first quarter.

The slowdown would be pronounced in the first half, while the second half should find support from monetary easing, consumption and statistical low-base effect.

Agricultural terms of trade are also expected to improve with a pick-up in food inflation. In addition, farmers would benefit from income transfer of Rs 6,000 per year announced by the Centre, and farm loan waivers in a few states.

Policy action looks attuned to consumption than investment demand, which means consumption will be the first to ascend as the tide turns.

But all that might not be enough to pitchfork growth this fiscal to, or above, the past 14-year average of 7% per annum.

So what is behind the slackening?

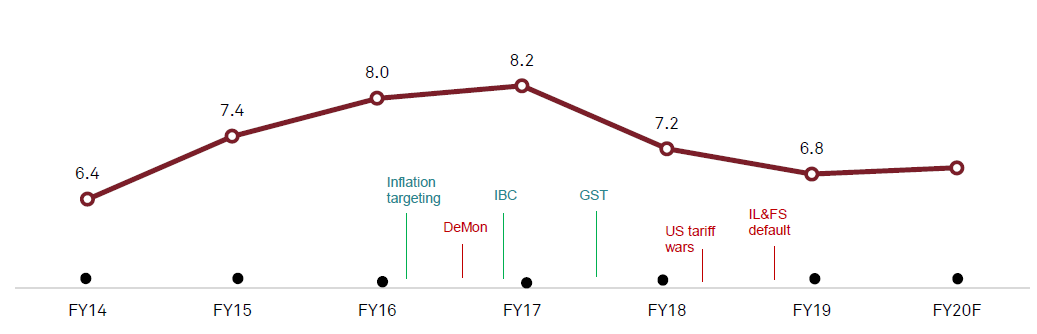

GDP grew at an impressive 8.2% in fiscal 2017, the fastest in a decade. Then a cyclical downturn got triggered because of disruptions wrought by policy initiatives and reforms, and rising global uncertainty stemming from trade disputes.

Weak global growth and falling trade intensity shrank India’s overall exports pie, and a gradual pick-up in crude oil prices fanned further headwinds. The rollout of Goods and Services Tax (GST) also had a knock-on effect on exports growth in the year of implementation because of delay in refunds to exporters.

Simultaneously, the farm front continued to flounder. Terms of trade for agriculture deteriorated in fiscals 2018 and 2019, and weak wage growth further affected rural incomes.

In all that time, public sector banking also remained incapacitated, primarily because of rising bad loans.

The onset of the non-banking financial company (NBFC) crisis in September 2018 aggravated the situation. Given that NBFC penetration is high in certain household consumption segments, the stress that ensued further impacted demand.

With access to funding becoming challenging and NBFCs caught up in managing liquidity, their growth halved to a multi-year low in the second-half of last fiscal, and remains impacted.

On the bright-side, banking sector non-performing assets (NPAs) are expected to decline anew to ~8% by March 2020, given lower accretion and increased recoveries. Credit growth should also grind up to 14%, the highest in five fiscals. Seasoning of retail portfolio and performance of the small and medium enterprise (SME) portfolio after the restructuring period will be the key monitorables.

Growth for NBFCs, mainly in the retail segment, is expected to pick up gradually. Also, NBFCs have used this opportunity to correct their asset-liability mismatches, and have reduced reliance on short-term market borrowings, which is a structural positive for the sector.

At the same time, funding access has not normalised for the sector, and asset quality risks in the wholesale book, especially developer funding, have increased.

Also, corporate revenue is set to grow at a slower 7.5-8.0% this fiscal, reversing the trend of double-digit growth in the past two fiscals.

A trifecta – of spurt in cost of compliance because of changes in regulation, tightening liquidity, and moderating income growth – is expected to impact sales volume in the automobiles sector. And how farm incomes pan out will weigh on rural demand-driven segments.

In other words, most consumption segments will pull revenue growth into single digit this fiscal. And weak prices of commodities such as steel and crude oil would exacerbate the pain.

As for industrial capex, it would remain moderate given the weak demand. Over the past few years, infrastructure investments (including public and private) have driven capex. But over the next three years, lower spending, such as on roads, is expected to drag growth in infrastructure investments to ~6% compound annual growth rate (CAGR) over the next three fiscals compared with 10% in the last three fiscals.

With public spending continuing to dominate investments, funding will remain a monitorable. This is also important because entities behind major infrastructure investments such as the National Highways Authority of India have run up debt significantly in the past few years.

And how has policy responded to the ructions?

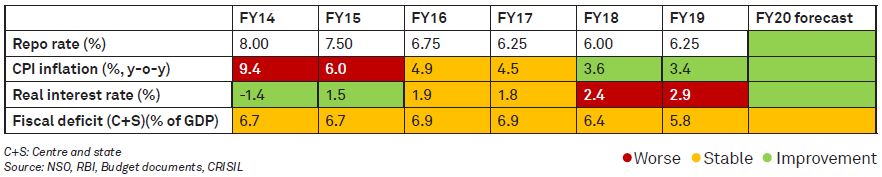

Monetary policy has focused on inflation control ever since the inflation targeting framework was adopted. To be sure, given our history, high core inflation rates, and the difficulty in assessing inflation (it has surprised on the downside), caution was warranted on rate cuts because of the chance of a spike in high real interest rates. In hindsight, however, one could say policy was tighter than warranted by the inflation trajectory. To boot, transmission of rate cuts is also chronically sluggish.

Fiscal policy, on the other hand, has had low wherewithal to pump the prime, given the glide path set out by the Fiscal Responsibility and Budgetary Management Act.

The upshot? GDP growth falling to a 20-quarter low of 5.8% in the last quarter of fiscal 2019. If it’s any consolation, in the last seven fiscals, there have been seven instances when quarterly GDP growth fell below 6%.

The crucial question, therefore, is whether a trough is in sight.

Given the fiscal constraints, public spending is unlikely to have the heft to pull growth above 7%.

And some of the recent, and much-needed, reforms would pay off only over the medium term.

There would, therefore, be some near-term onus on monetary policy to stimulate growth. But how effective that can be is the big question.

So fingers crossed for now.

Anatomy of a slowdown

Amid the murmur of slowdown and growth forecast cuts, two questions are gaining decibels: What is hampering growth? Is the slowdown here to stay?

Here’s what we think:

The problem statement

GDP growth slowed to a five-year low of 6.8% in fiscal 2019 on-year, with the last quarter growth printingat 5.8%. Growth has been on a cyclical downturn since fiscal 2017, when it peaked at 8.2%. Disruptions andreforms marked the economy, particularly after 2016. These, together with adverse exogenous developments,have impacted growth.

Five things that shaped today’s economy

We explain the past growth trajectory and predict this fiscal’s path through five frames:

Disruptions and reforms - led to a drift down

- The three major disruptions since 2016 were: Demonetisation, United States (US)-China trade spat, andthe Infrastructure Leasing and Financial Services (IL&FS) debacle. Fiscal 2017 was synonymous withdemonetisation. Just as its effects were petering out, came the NBFC credit crunch in 2018, causedby the IL&FS crisis. By 2018-end, weakening global trade and GDP growth, led by US-China tariff wars,had caught up

- The three key economic reforms were: Adoption of inflation targeting framework by the Reserve Bankof India (RBI), and implementation of the GST and the Insolvency and Bankruptcy Code (IBC). Reforms,in general, could be short-term disruptive and long-term supportive. We saw the first part happenaround the GST. Though not inflationary, it did disrupt export growth in 2017, when global growth was atits highest since the financial crisis

- In fiscal 2020, we expect to see continued streamlining of GST and IBC processes. That should graduallyrelay into greater efficiency and growth over the next few years

Growth as a steeplechase

Monetary and fiscal policies – tied down by targets

- Monetary and fiscal policies are two key instruments to fight a cyclical downturn

- However, the fiscal and monetary authorities have, by and large, chosen restraint over using these instruments to stoke growth

- Inflation control has preoccupied monetary policy since targeting was adopted. In hindsight, sub-target inflation rates could have afforded a more accommodative stance. But given the history of high inflation, high core inflation rates, and difficulty in assessing inflation (which surprised everyone on the downside), caution was exercised on rate cuts, leading to high real interest rates

- Fiscal policy, too, has not been used to pump-prime the economy. The combined fiscal deficit of the Centre and the states stands high. The government intends to pare it down this fiscal, despite growth headwinds. To be fair, there is hardly any fiscal wiggle room with the government, and that justifies its prudent fiscal stance

- In calendar 2019, though, monetary policy has turned growth-supportive. The Monetary Policy Committee slashed the repo rate thrice by 25 basis points (bps) each, and changed the stance to ‘accommodative’. However, anaemic transmission means growth will lift off with a lag

- We expect the rate cuts to transmit by the second half of fiscal 2020. But the fiscal policy’s ability to pump- prime the economy will remain constrained, owing to high debt levels

Combined fiscal deficit and real interest rates are high

Global environment - half empty, half full

- The global growth environment is gloomy:

- Global growth and trade intensity have declined post the global financial crisis, making export-led growth a more distant possibility

- At this juncture, the risks to the global economy are tilted to the downside because of uncertainty around US-China trade war and the Brexit outcome

- Crude prices were favourable in the first three years of National Democratic Alliance (NDA) I, which created tailwinds for India’s growth, inflation, and fiscal deficit. However, that has moved up since fiscal 2018,reversing the advantage

- The global scenario holds out a mixed bag for this fiscal:

- Slowing global growth and strong rupee are bad for exports; escalation of the US-China trade war could create further downside risks

- Softening policy stance in advanced countries would lead to capital inflows, currency appreciation, and support soft interest rate policy

- Oil prices will be shaped by the interplay of two opposite forces: geopolitics offsetting the price-depressing impact of weak global growth

The world offers little comfort

Financial sector – frictions resurface

- The banking sector’s NPA ratio worsened throughout the UPA-II term and is still quite high

- No sooner did the NPA ratio started improving in fiscal 2019, the NBFC stress started building up

- Stress in NBFCs percolates faster, owing to greater interconnectedness (to mutual funds, banks, and corporate sector) vis-à-vis public sector banks

- For fiscal 2020, bank credit growth might improve somewhat, but NBFC credit looks subdued, despite the partial guarantee scheme announced in the Union Budget 2019-20

Farm sector – pines for level-playing field

- Worsening agricultural terms of trade has squeezed farm income

- Non-food inflation continued to surpass food inflation in the past two years, amounting to income transfers from rural to urban areas

- Farm income could get a leg-up from the government’s income transfer scheme, and a rise in food prices would boost the terms of trade

Financial sector still nursing its wounds, farmers’ woes aren’t done yet

Parts of the problem

GDP is the sum of consumption, investment, government spend, and net exports. Here, we consider consumptionand investment, and exports. What has been their role in the current slowdown? This section breaks it down, andjoins the dots to fiscal 2020.

Consumption

The chips are down as income, credit and sentiment slip

Consumption has been the bulwark of growth in recent years.Hence, a slowdown in consumption has triggered slower GDP growth. Sluggishness in rural demand, dent in exporters’ incomes, and tighter credit flow to the retail sector in wake of the NBFC crisis started telling on consumption demand, especially in the second half of fiscal 2019. Though, for the fiscal as a whole,private consumption growth was higher at 8.1% on-year compared with 7.4% in fiscal 2018, consumption suffered in the second half. Growth slid to 7.7%; nearly 100 bps lower than in the first half.

Over the past few years, households dipped into their savings and leveraged themselves to finance consumption. Higher leverage played a critical role in supporting the consumptionboom. However, post the NBFC credit crunch, credit has become somewhat inaccessible to the riskier customer profile, somewhat constraining households’ ability to spend. The box Savingsinvestment conundrum (Annexure 1, Page 41) delves deeper into implications of a savings slowdown.

Foresight