Interest rates

RateView : CRISIL's outlook on near-term rates

January 2019

Executive summary

Yields on the 10-year benchmark government security (G-sec) opened December 2019 at 6.49%, rising to a high of 6.80% at near-about the mid-month mark. Yields reversed course thereafter, closing the month at 6.56%, which was marginally outside CRISIL’s forecast of 6.60-6.80%. The fall in yield was because of the Reserve Bank of India’s (RBI) surprise announcement of ‘operation twist’.

With expectations of a rate cut not fructifying, the 10-year benchmark G-sec rose up to the mid-point of the month. The Monetary Policy Committee (MPC) kept rates unchanged with an eye on inflation. Also hardening the yields were rising US treasury rates and crude oil prices, and heavy selling by foreign investors. A further tailwind was from fears of a sovereign rating downgrade - S&P hinted at downgrading India’s rating if economic and growth conditions did not improve.

The consumer price index (CPI) print of 5.54% for November 2019, which was a 40-month high, sustained the upward trajectory, with the yield ending the fortnight at 6.79%, or ~30 basis points (bps) higher than the start of the month.

In the second half of the month, the RBI’s announcement of operation twist brought cheer to the market. The central bank’s announcement of open market operation (OMO) purchases of the 10-year benchmark G-sec and simultaneous sale of shorter tenure (2020 maturity) securities with the objective of lowering term premiums pulled down the 10-year G-sec to 6.60%.

The yield slid some more following a second round of operation twist. A further decline was arrested because of profit-booking by investors and rising crude oil prices, with the 10-year benchmark G-sec ending the month at 6.56%, 9 bps higher than previous month’s closing.

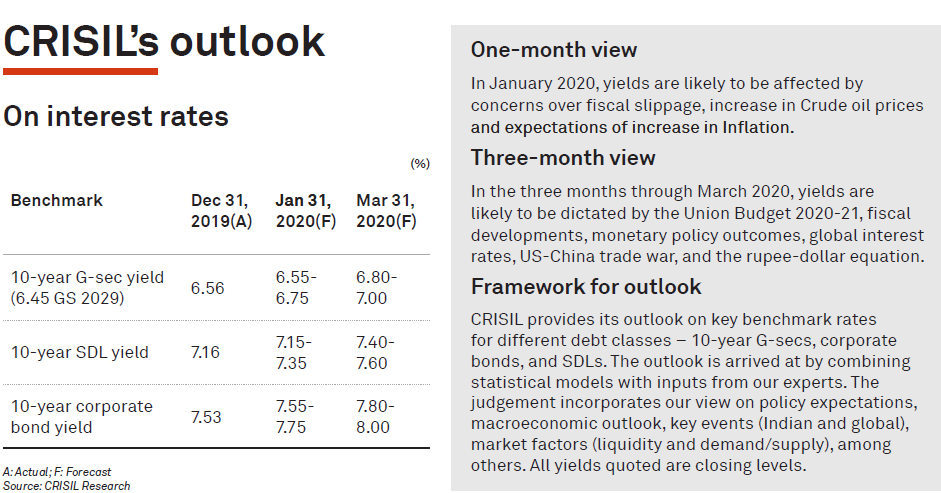

The spread over the new 10-year benchmark G-sec was 97 bps for corporate bonds and 60 bps for state development loans (SDLs). CRISIL’s view for the 6.45% G-sec 2029 yield is 6.55%-6.75% for January-end and 6.80%-7.00% for March-end. Spreads for corporate bonds and SDLs are expected to remain steady over the next three months.

Analytica