Partial collections + low disbursements = some liquidity respite for NBFCs

Availability of bank moratorium will provide significant support at this juncture

Sucess Dialog

This is added to your favourites.

Warning Dialog

This is already added to your favourites.

sorry something went wrong.

Liquidity covers1 of non-banking financial companies2 (NBFCs) have not depleted significantly over the past two months, CRISIL’s analysis3 of the NBFCs it rates indicates. However, fund-raising continues to be a challenge for most NBFCs because investors remain risk-averse. With debt repayments remaining high in the near term – especially June 2020, how NBFCs manage the refinancing risk will be a key monitorable. In the milieu, availability of moratorium on loans NBFCs had taken from banks will offer them material liquidity support.

The liquidity covers have not depleted significantly because NBFCs managed some collections in April and May, which varied depending on the segment of operations. Negligible disbursements also helped prop up liquidity covers to some extent, compared with earlier estimations.

CRISIL had earlier indicated (please refer to our credit alert of April 10: Moratorium non-availability for NBFCs – A double whammy) that liquidity covers for NBFCs could reduce in the event of weak incremental funding, collections and limited moratorium on their bank borrowings.

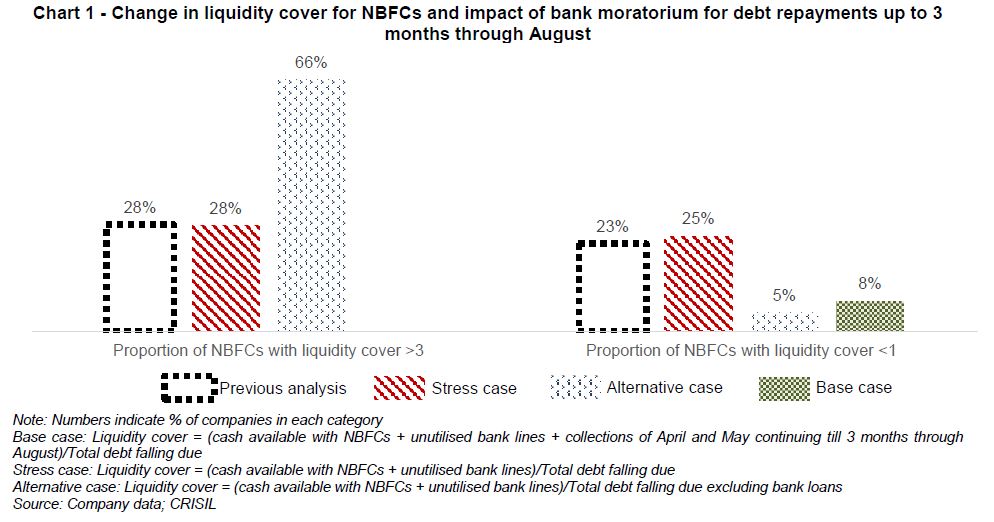

For the latest analysis, CRISIL looked at three scenarios: (i) a base case, where it is envisaged that collections in the next few months will be similar to April-May levels without any moratorium on liabilities; (ii) a stress case, where collections are nil and there is no moratorium on liabilities, leading to depletion of liquidity cover; and (iii) an alternative case, where NBFCs get benefit of moratorium on their bank loans but there being no collections. The inferences from these scenarios are presented in the table below.

In the base-case scenario, the proportion of NBFCs with liquidity cover of less than 1 time (low liquidity cover4) will be 8% during the three months through August. Our earlier analysis had estimated 23% of NBFCs will have low liquidity cover in this period.

However, in the stress-case scenario, the proportion of companies with low liquidity could go up to 25%, underscoring the importance of NBFCs ratcheting up collections.

On the collections side, the calibrated lifting of lockdown restrictions, coupled with extension of moratorium by the Reserve Bank of India (RBI) by another three months, has raised the spectre of more of NBFC borrowers opting for moratorium and has heightened the risk of credit-culture vitiation.

Factoring the lumpiness of repayments in June – typical to quarter ends – and potential impact on collections due to extension of moratorium, support from banks will be crucial for a number of entities.

Says Krishnan Sitaraman, Senior Director, CRISIL Ratings, “Despite cash outflow owing to debt repayments, a combination of partial collections, incremental funding, and negligible disbursements has supported the liquidity levels of NBFCs. But June is crucial with nearly Rs 1.25 lakh crore of repayments, which is half of the ~Rs 2.5 lakh crore due through August. However, if banks were to offer moratorium on them, the proportion of NBFCs with low liquidity cover reduces significantly to just 5% from 25% envisaged in our stress-case scenario.”

In terms of incremental funding, capital market issuances have dropped substantially, with investments by mutual funds– a key investor segment – in NBFC debt plunging to the lowest level in more than two years.

The securitisation route, too, has seen very few transactions consummating in the past few months due to concerns over asset quality and lack of granular track record of collection efficiency after the pandemic onset.

At the same time, the government and the RBI have also announced a number of measures to ease fund flow to the sector; their effectiveness though is yet to manifest.

NBFCs have been a pivotal part of the Indian credit ecosystem, given their last-mile connect and expertise in tapping unbanked borrowers as well as micro, small and medium enterprises. But with a predominantly wholesale resource base and lack of access to systemic liquidity support, NBFCs are more vulnerable to liability-side stress compared with banks. Further, any stress in the NBFC sector can cascade into funding deficiencies in the segments they lend to, which can then morph into systemic issues.

That is why support from banks for NBFCs will be all the more crucial in the context of stability of the financial system at large. One form of this support in the current context would be availability of bank loan moratorium for NBFCs which can substantially improve their liquidity covers (see chart 1 below).

CRISIL continues to closely monitor the credit profiles of its rated NBFCs and will take appropriate rating action.

1 Measured as “(cash available with NBFCs + unutilised bank lines) / debt falling due”. Debt falling due for the next 3 months is excluding bank loans where NBFCs have received written confirmation from bankers on getting the moratorium 2 Comprising NBFCs, housing finance companies, microfinance institutions, but excluding government-owned non-banks 3 Analysis covers CRISIL-rated investment-grade NBFCs, which constitute around 90% of industry assets under management (AUM) 4 Low liquidity cover indicates that collections, availability of moratorium on liabilities, access to additional funding and/ or external support are important to meet debt obligations in time

Mumbai

Mumbai