Mumbai

Mumbai

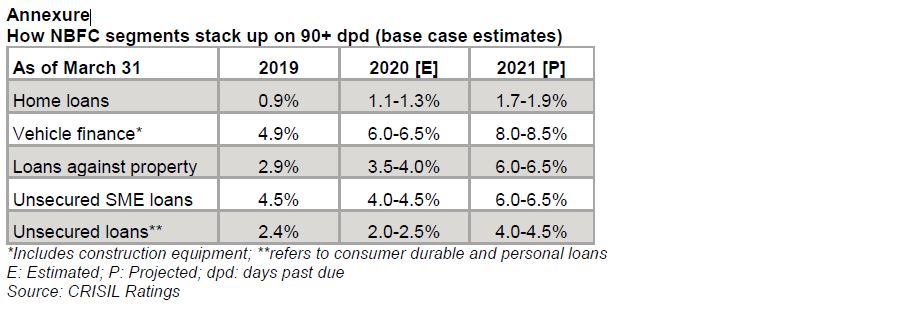

[1] NBFCs including housing finance companies, but excluding government-owned NBFCs

[2] Micro, small and medium enterprises: includes Loans against property (LAP) and unsecured SME loans

Subscribe for our press releases

Media relations

Saman Khan

Media Relations

CRISIL Limited

D: +91 22 3342 3895

M: +91 95 940 60612

B: +91 22 3342 3000

saman.khan@crisil.com

Krishnan Sitaraman

Senior Director - CRISIL Ratings

CRISIL Limited

D: +91 22 3342 8070

krishnan.sitaraman@crisil.com

Ajit Velonie

Director - CRISIL Ratings

CRISIL Limited

D: +91 22 4097 8209

ajit.velonie@crisil.com