Mumbai

Mumbai

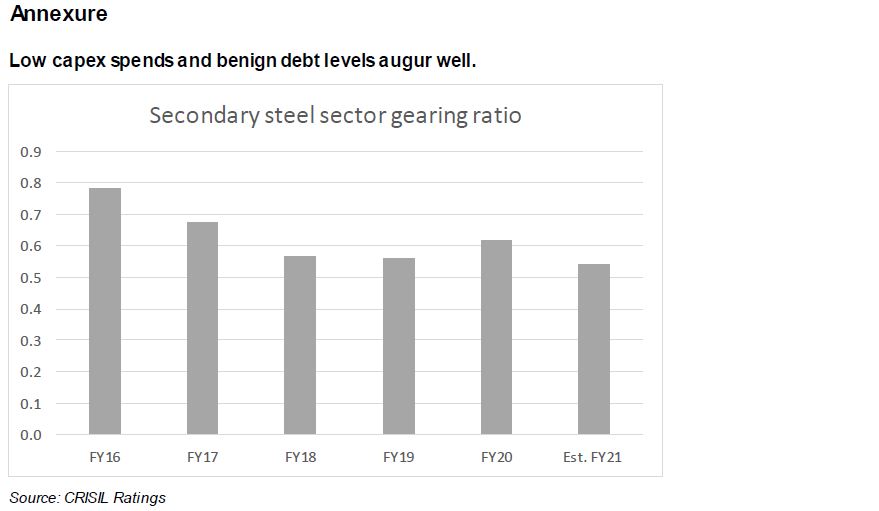

1 Debt to equity ratio

2 Earnings before interest, depreciation, taxes and amortization (EBIDTA) divided by interest & finance cost

Subscribe for our press releases

Media relations

Saman Khan

Media Relations

CRISIL Limited

D: +91 22 3342 3895

M: +91 95 940 60612

B: +91 22 3342 3000

saman.khan@crisil.com

Mohit Makhija

Director - CRISIL Ratings

CRISIL Limited

B: +91 124 672 2000

mohit.makhija@crisil.com

Jaya Mirpuri

Director - CRISIL Ratings

CRISIL Limited

B: +91 22 3342 3000

jaya.mirpuri@crisil.com