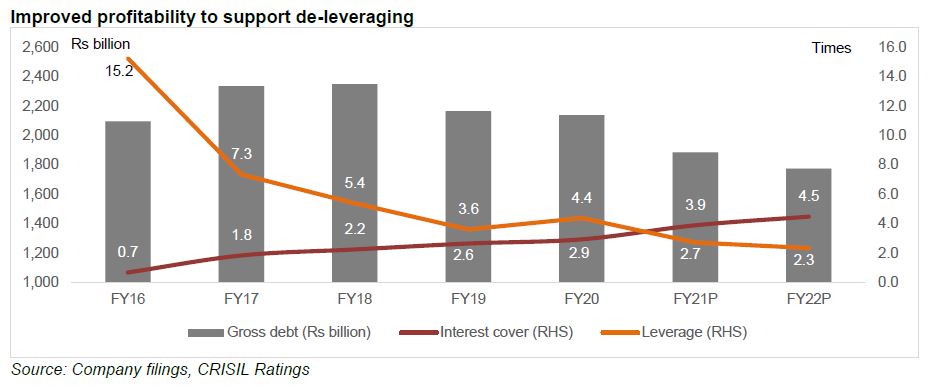

Primary steel producers are expected to reduce debt by ~15%, or ~Rs 35,000 crore, between fiscals 2021 and 2022, using the higher operating profits generated for prepayment.

That, and a partial deferral of capex this fiscal will strengthen the balance sheets and credit metrics of five primary steel producers, which account for 55% of domestic production1.

Domestic demand recovered strongly in the second half of this fiscal, growing ~10% between October and January versus a 30% on-year fall in the first half. Consequently, demand contraction will be less than 10% for the whole of this fiscal. Higher infrastructure spending by government, and recovery in residential real estate are expected to improve steel demand by 10-12% next fiscal.

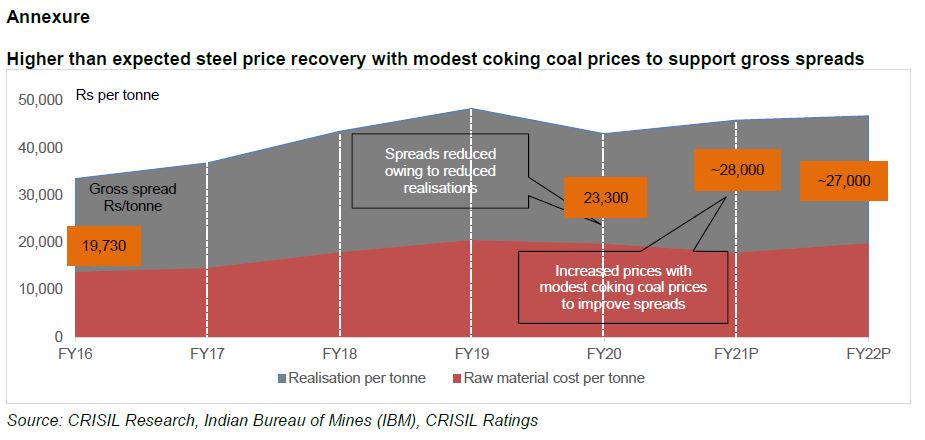

Domestic hot-rolled coil (HRC) prices rallied to a multi-year high of ~Rs 56,000 per tonne in February from Rs 39,200 per tonne in March 2020 as demand improved amid iron-ore supply constraints and high global prices. Since last month, however, prices have moderated with iron-ore supplies improving, and also because of the reduction in customs duty2 announced in the Union Budget.

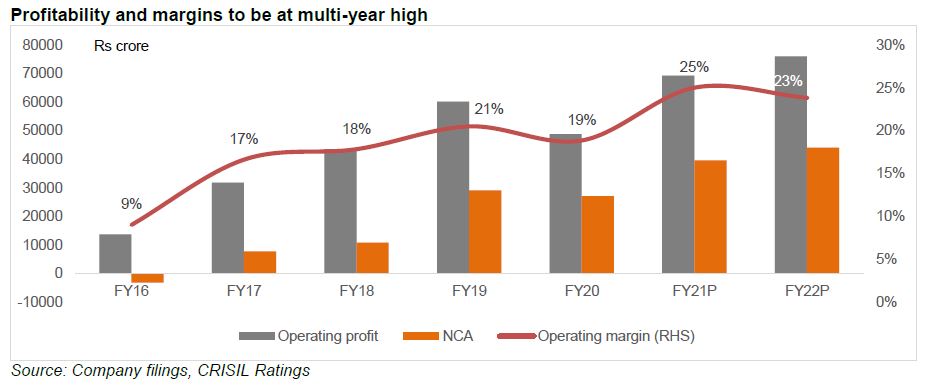

Says Manish Gupta, Senior Director, CRISIL Ratings, “So while the tailwinds to realisations from higher input costs and global prices could abate going forward, domestic demand growth would provide an offset. Consequently, realisation next fiscal may still be ~15% higher than the average of the past five years. That, along with rising volumes and moderate coking coal prices would mean healthy operating margins of ~23% next fiscal, compared with ~25% likely this fiscal.”

Operating margins had plunged to ~9% in the previous steel downcycle of fiscal 2016. Since then, what has helped are improved raw material linkages, and better operating efficiencies of stressed assets (following consolidation with stronger peers).

Cash accruals3 could surge over 40% on-year to Rs 40,000 crore this fiscal, and rise another 10% next fiscal. That, and a reduction in capex this fiscal (to conserve cash and pare debt) will fortify financials amid the pandemic uncertainties.

Says Naveen Vaidyanathan, Associate Director, CRISIL Ratings, “The five steel makers could cut ~ Rs 25,000 crore of debt this fiscal. Next fiscal, despite capex rising ~15%, they can slice debt by another Rs 10,000 crore. That would drive a sharp improvement in credit metrics with financial leverage (ratio of debt to Ebitda) declining below 2.5 times next fiscal compared with above 4.0 times in fiscal 2020.”

Any fall in steel prices due to weaker global demand and higher supplies, especially from China, and the second wave of Covid-19 afflictions impacting domestic demand will bear watching.

1 Include Jindal Steel & Power Ltd, Tata Steel Ltd (including Bhushan Steel Ltd), JSW Steel Ltd, Steel Authority of India Ltd and Arcelor Mittal Nippon Steel India Ltd (erstwhile Essar Steel India Ltd)

2 Budget 2021: basic customs duty reduced to 7.5% from 12.5% on semis/flat steel products, & from 10% on long steel products

3 Accruals is defined as net profit + depreciation - dividend

Mumbai

Mumbai