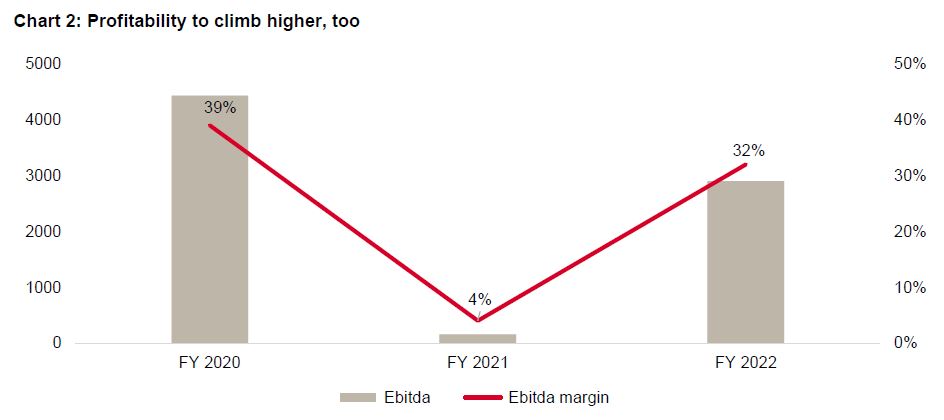

A material increase in tariff will help lift the aggregate operating profit1 of four private airports – in Delhi, Mumbai, Hyderabad and Bengaluru – to ~65% of their pre-pandemic levels (of fiscal 2020), next fiscal. This fiscal, their operating profits are expected to plunge 90% because of a vertical drop in passenger traffic.

These airports accounted for over 90% of the air passenger traffic handled by private airports in India, and ~55% of all such traffic in calendar year 2020.

Three of these four airports are likely to see their aeronautical tariffs (levied on the passenger traffic, cargo, airport landing & parking fee, etc.) more than double on an aggregated average, from current levels. This is because the airport regulations allow the airports to get a fixed regulated return on the capacity addition being done in the control period2, charged through tariffs. Further, regulations also allow a true-up in the tariff to compensate for the loss in aeronautical revenue due to lower-than-expected traffic over the previous control period.

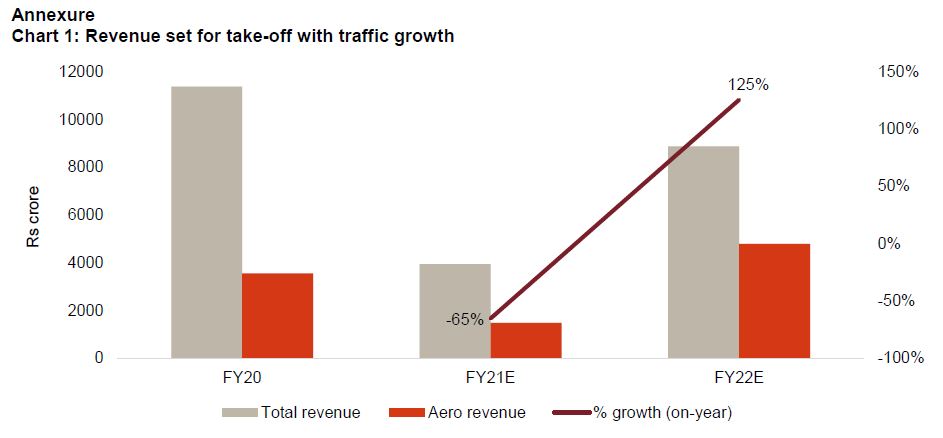

About one-third of the anticipated hike in tariffs is to compensate for the loss in aeronautical revenue due to lower-than-expected traffic over the last and current fiscals. The remaining two-thirds is to provide a fixed return on the capacity addition done in the current tariff control period of 5 years.

Says Manish Gupta, Senior Director, CRISIL Ratings, “The tariff hikes will help aeronautical revenue bounce back next fiscal to 1.3 times of fiscal 2020. However, these form only half of the overall revenue of these airports. The other half – non-aeronautical revenue3 – remains sluggish due to slow pick-up in passenger footfalls despite some relaxation in people movement, and low propensity of passengers to spend in the airport ecosystem at present. Consequently, overall revenue next fiscal will be lower than in fiscal 2020.”

Airports’ slow revenue recovery will impact their operating profits which at best will reach 65% of their pre-pandemic levels in fiscal 2022. This is contingent upon timely and adequate grant of tariff hikes based on petitions filed with the regulator by the airports.

Airports are regulated monopolies and will therefore see traffic recover eventually, but the pace of recovery remains uncertain and dependent upon the Covid-19 wave and recovery in the travel preferences of people, especially for cross-border journeys.

Says Ankit Hakhu, Director CRISIL Ratings, “Our estimates assume traffic may fully recover only by fiscal 2023, actual tariff hike on average be around 115% of current levels and provided during the next 3-4 months for airports where filings have been made. A significant delay or lower-than-expected tariff hikes would weaken debt-servicing metrics and credit profiles.”

Most airports have built cash buffers through upfront borrowing or push down of debt maturities via refinancing, or surplus build-up from excesses from previous tariff control periods. We estimate that such liquidity buffers, including working capital lines, would be adequate for up to four quarters4 of debt servicing.

This, along-with airports’ regulated business model and operating exclusivity, support ratings in adequate and high-safety categories for most airports. That said, final decision by regulators on the quantum of hikes and timeliness remains a critical monitorable.

1 Operating profits are earnings before interest, tax, depreciation and amortisation (Ebitda).

2 Approval for aeronautical revenue comes through tariff orders, which judge entitlement in 5-year block periods, called control periods. Lower or higher collections get adjusted or trued up/ down in the next block period.

3 Revenue through duty free, lounge revenue, retail and rental revenue.

4 Debt servicing excludes any bullet debt repayment that is expected to be refinanced.

Mumbai

Mumbai