Interest rates

RateView : CRISIL's outlook on near-term rates

December 2019

Executive summary

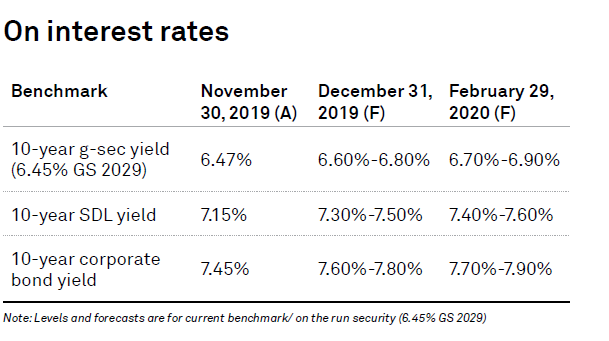

Yield on the 10-year new benchmark government security (g-sec) rose from 6.45% at the beginning of November to a high of 6.57%, before coming down to 6.52% at mid-month and closing the month at 6.47%, within CRISIL’s forecast range of 6.35%-6.55%.

G-sec yields began November with an upward bias, due to uncertainty about the US-China trade deal, a rise in crude oil prices and an increase in US Treasury rates. Fears about the possibility of fiscal slippage in India dampened the market participants’ risk appetite. Yields hardened further mid-month after Moody’s downgraded India’s rating outlook from ‘Stable’ to ‘Negative’, fuelling fears about FPI (foreign portfolio investment) outflows; the 10-year benchmark g-sec yield went up 12 bps to 6.57% from the beginning of the month on this. The 10-year yield ended the first fortnight at 6.52%, despite a higher CPI print at 4.62% (the highest level in the past 16 months) versus 3.99% in the previous month and above the Reserve Bank of India’s (RBI) comfort level of 4%. Higher expectations about a rate cut by the RBI’s Monetary Policy Committee (MPC) in the upcoming policy cooled down yields.

Yields on g-secs remained stable within the 6.46%-6.51% range in the second half of the month. The Cabinet Committee on Economic Affairs approved the disinvestment of five PSUs, providing some cushion to the Central government’s strained revenues. The market’s mood turned downbeat ahead of the comment by the RBI governor Shaktikanta Das on the stressed fiscal positions of the Centre and states. Yields remained range-bound on continued expectations about a rate cut (because of poor GDP forecast estimates for the second quarter of fiscal 2020) and profit booking by market participants. However, they closed the month at 6.47%.

The spread over the new 10-year benchmark g-sec was 98 basis points (bps) for corporate bonds and 68 bps for SDL (statedevelopment loan). CRISIL’s view for the 6.45% GS 2029 yield is 6.60%-6.80% for December-end and 6.70%-6.90% for Februaryend. We expect the spreads for SDLs and corporate bonds to remain steady over the next three months.

One-month view

In December, yields are likely to be affected by fiscal developments, monetary policy outcomes (Indian and global central banks), US-China trade war, minutes of the MPC’s meetings, crude oil prices, global interest rates and FPI flows.

Three-month view

In the three months through February, yields are likely to be affected by the expectations from the Union Budget for 2020-21 and the next MPC meeting, fiscal developments, global interest rates, US-China trade war, the rupee-dollar equation, and global central banks’ policy stance.

Analytica